Goldiam stock surged 12x, but does it still hold rerating potential? | Smart Stocks News

For centuries, diamonds have been symbols of pride and wealth — and for good reason. Their rarity and high price made them coveted possessions, often displayed as markers of affluence.

But new technology is challenging that legacy. The rise of lab-grown diamonds (LGDs), which replicate the properties of natural diamonds at a fraction of the cost, has shaken up the industry. This shift has created a growing divide between those who swear by natural diamonds and those embracing these more affordable alternatives.

The impact is undeniable. Over the past decade, demand for LGDs has surged. To compound the issue, the gems and jewellery industry is grappling with declining prices of natural diamonds due to this customer shift. Falling diamond prices further dented its image.

In 2023 alone, LGDs quadrupled their market share, climbing to 15.4%. With this rapid growth, companies are rushing to establish themselves in this booming sector.

Among the many players, one name stands out: Goldiam International. The company has attracted attention not just for its ambitious plans but also because prominent investor Ramesh Damani holds a 1.58% stake — a detail that hasn’t gone unnoticed.

As Goldiam gears up for a significant expansion in 2025 and beyond, one question remains: What’s its master plan? Let’s find out.

Betting big on LGDs

Goldiam began its journey in 1986 as a diamond exporter, specialising in cutting and polishing stones for the global market. As the industry evolved, the company shifted focus to value-added diamond jewelry and set up operations in the US to sell directly to international retailers. Recognising the growing popularity of lab-grown diamonds (LGDs), Goldiam made an early entry into the market. Today, it is a leading LGD supplier with an omnichannel sales strategy designed to stay in sync with changing market trends.

Story continues below this ad

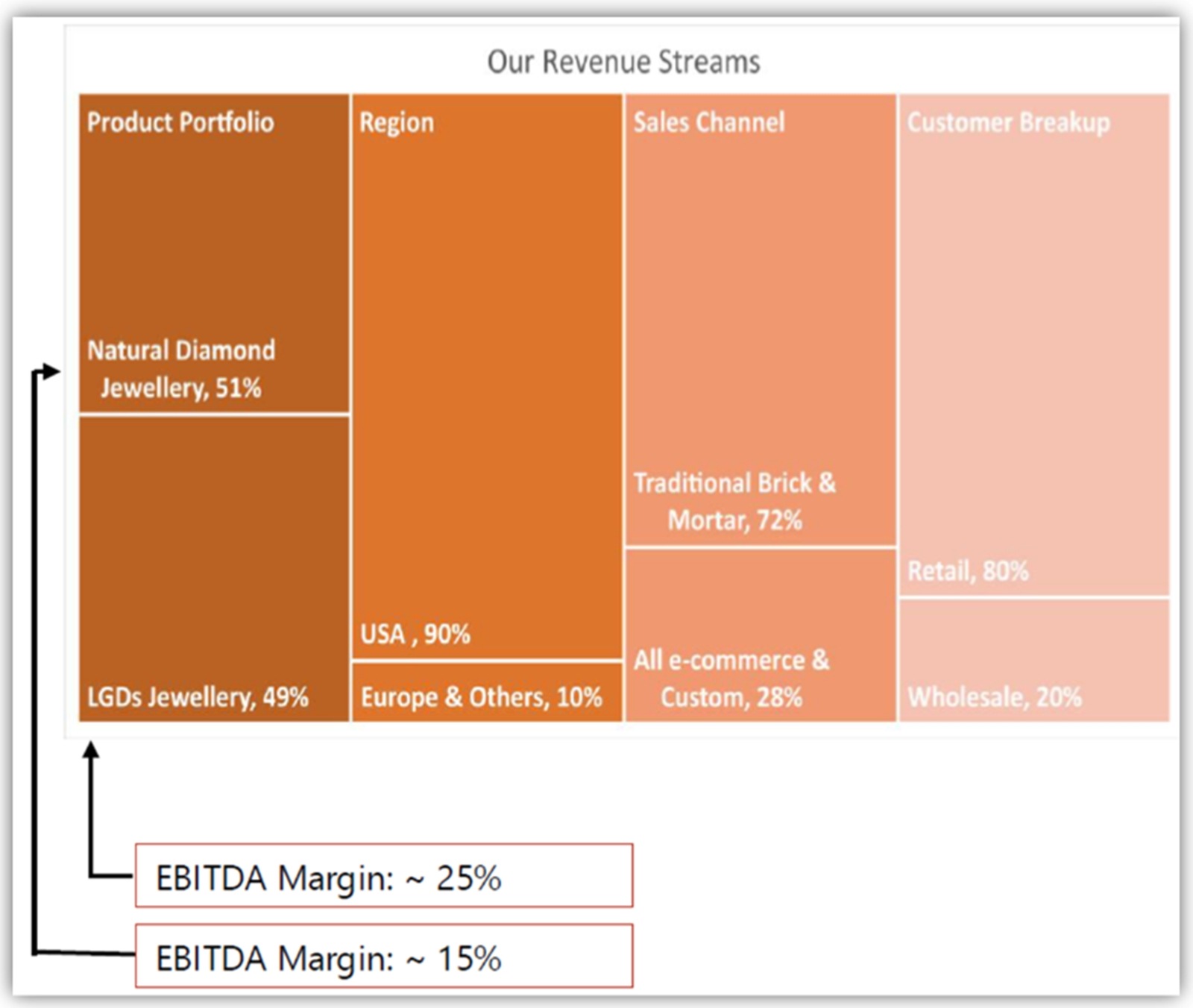

LGDs contribute 80% to Goldiam’s revenue, with 49% of its revenue coming from this segment. However, the majority of its revenue still comes from exports to the US, with limited domestic sales — a gap the company is now actively working to bridge, with its brand ORIGEM.

49% of Goldiam’s Revenue Comes from LGD. (Source: Q3FY25 Investor Presentation)

49% of Goldiam’s Revenue Comes from LGD. (Source: Q3FY25 Investor Presentation)

ORIGEM operates both physical stores and an online platform.

As of January, the company has opened four stores under the company-owned, company-operated (COCO) model. These stores have already achieved monthly sales of ₹3 million, with an average selling price of ₹40,000-50,000 per piece. The company is focusing on opening these stores in micro markets with high purchasing power.

In the next 3-5 years, the company plans to open 150-200 new stores, with the goal of doubling the ORIGEM business over the next 4 years. The company will finance this expansion through internal accruals as its cash and cash equivalents stand at Rs 2.75 billion.

Story continues below this ad

The company believes that this expansion will help it increase LGD Jewellery’s contribution to its total revenue to 20%, amounting to ₹0.9-1.2 billion over the next four to five years.

Goldiam’s EBITDA margin on LGD sales is 25%, well above the 15% from natural diamonds. As LGD sales make up a larger share of total revenue, both growth and profitability are likely to rise.

Goldiam also has a strong order book of ₹1.75 billion for supplying LGDs.

The company continues to maintain a strong global presence. It generates 51% of its revenue from international markets, with the US contributing 90% and Europe and other regions contributing 10%.

Story continues below this ad

It exports designer luxury diamond jewellery to major retailers, department stores, and wholesalers across the US, tapping into a $3-3.5 billion export market.

The company is also enhancing its e-commerce presence with a dedicated website and plans to maintain a 25-30% revenue contribution from online sales.

To sustain growth over the next 3-5 years, Goldiam is exploring new geographies beyond the US. It plans to enter new markets like Australia and the Middle East, where rising disposable incomes and strong demand for luxury goods present significant opportunities.

The bottom line: How it adds up

Goldiam has shown consistent growth over the last five years, with its revenue, profits, and margins maintaining a healthy upward trajectory.

Story continues below this ad

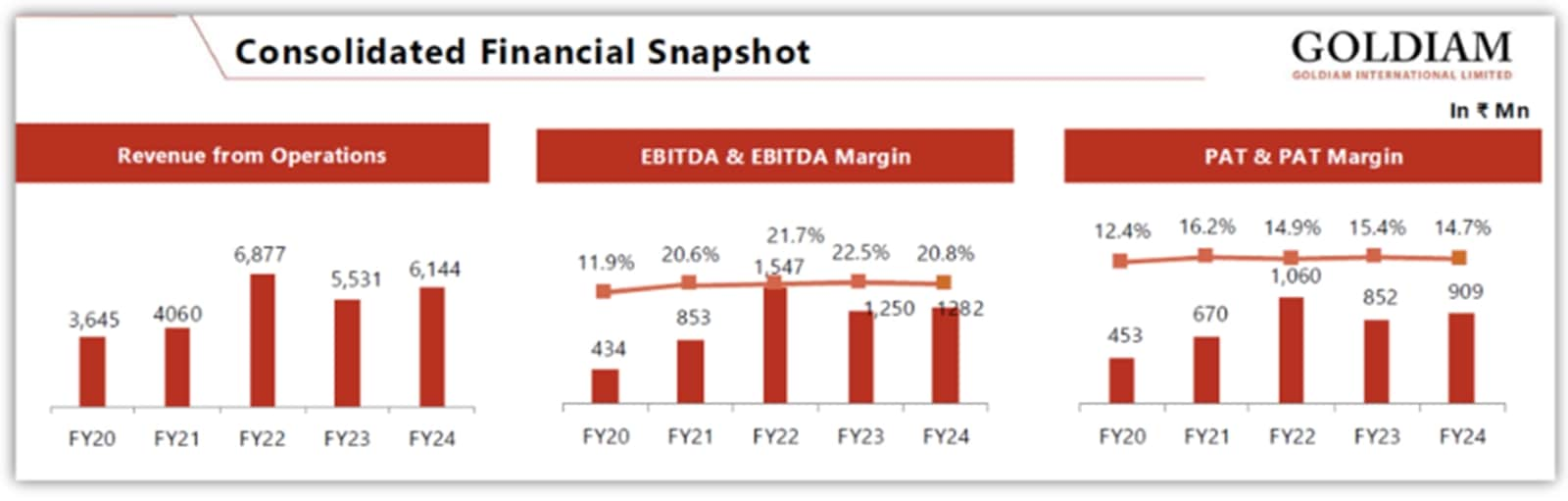

Its revenue has grown at a compounded annual growth rate (CAGR) of 16% to ₹6.14 billion in FY24, a 13% increase compared to the last year. Its profit increased at a CAGR of 20% to ₹0.91 billion in FY24.

Goldiam’s Revenue and Profit has Grown at 16% and 20% CAGR. (Source: Q3FY25 Investor Presentation)

Goldiam’s Revenue and Profit has Grown at 16% and 20% CAGR. (Source: Q3FY25 Investor Presentation)

This has allowed earnings before interest, taxes, depreciation, and amortisation (EBITDA) to expand 2.9 times to ₹1.28 billion. The EBITDA margin now stands at 20.8%, significantly higher than 11.9% five years ago.

Additionally, the company reported a robust return on equity of 14.8% and an impressive return on capital employed (ROCE) of 37%.

As a result of its strong growth, Goldiam’s share price has been re-rated.

Story continues below this ad

The share price has increased 12-fold to ₹402, driven by price-to-equity expansion from 7x to 39x.

Goldiam’s share price

Goldiam’s share price

Comparing Valuation

Despite this surge, Goldiam’s valuation remains significantly lower than industry leaders like Titan and Kalyan, which trade at P/E multiples of 89x and 82x, respectively.This potentially leaves more room for its stock price to rise if the company sustains its growth momentum.

However, the discount might also be justified. Titan and Kalyan operate diversified, time-tested business models with expansive retail footprints. In contrast, the LGD market is relatively nascent, with considerable uncertainty surrounding its future.

Story continues below this ad

Then, there is this issue of LGD’s price decline due to excess supply, which is a significant concern. If this continues, Goldiam’s margins may be severely impacted. And if LGD were to become truly commoditised, this could also affect demand and growth.

In its Q3FY25 conference call, the company said that LGD prices have stabilised and that they do not expect the price to fall further. One will need to wait and see whether this plays out as the management expects.

The broader industry is thriving, with the global LGD market having more than doubled to about $25.9 billion in 2024, up from about $11 billion in 2011.

However, the Indian LGD market remains relatively small, currently valued at $2.7 billion.

Story continues below this ad

It will be interesting to see whether Goldiam’s LGD story retains its shine.

Note: We have relied on data from http://www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Madhvendra has been tracking equity markets for over seven years, combining his passion for investing with his expertise in financial writing.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.