Zomato triggers another war: Big brokerages take big opposing views | Smart Stocks News

The festive season came as a downer for Zomato and Swiggy. Their share prices fell by 25-30% from December 15 onwards as broader consumer demand slowed. The two stocks underperformed the Nifty 50 Index, which fell 6.6%. Zomato raised Rs 8,500 crore through a Qualified Institutional Placement (QIP) in Q3FY25, which changed the shareholding pattern. Foreign Institutional Investors (FIIs) stake reduced to 47.31% in December 2024 from 52.53% in September 2024.

While the overall market sentiment was bearish, one major reason that perhaps precipitated the fall in Zomato’s share price was analyst ratings. Jefferies downgraded Zomato’s stock to ‘hold’ in early January 2025 and reduced the price target from Rs 335 to Rs 275 due to rising competition in quick commerce.

On 22 January, it further reduced the price target to Rs 255 after Zomato hit the reverse gear on its consecutive profit growth in the last four quarters to register a decline. The company reported a 57.2% year-over-year (YoY) decline in its Q3 FY25 net profit to Rs 59 crore.

Analysts noted that Zomato’s growing capital spending in dark store expansion could accelerate revenue growth but delay profitability due to the high initial expense of new store opening.

Analysts react to Zomato’s Q3 earnings

Many other analysts joined Jeffries and reduced their price target on Zomato post earnings.

- Nuvama reduced price target from Rs 325 to Rs 300

- IIFL Securities from Rs 300 to Rs 250

- Nomura from Rs 320 to Rs 290

- Kotak Equities from Rs 305 to Rs 275

Macquarie had a bearish target of Rs 130, representing a 40% downside.

Even Morgan Stanley, which consistently increased its price target for Zomato from Rs 278 in August 2024 to Rs 355 in early January due to its focus on profitability and consistent growth, reduced its price target to Rs 195–Rs 215 levels. The brokerage sees an overhang on multiples as its price-to-earnings (PE) ratio crossed 300x.

Story continues below this ad

While most analysts reduced their price target after Zomato’s earnings, Bernstein maintained an ‘Outperform’ rating, with a target price of Rs 310. The international brokerage suggests that any dip in share price because of competition concerns presents a buying opportunity.

The takeaway from analysts’ reports

The keyword in all analysts’ reports is intensifying competition. Zomato leads quick commerce with a market share of 46%, followed by Zepto at 29% and Swiggy at 25%, according to Motilal Oswal’s report.

A hilarious but true story showcasing the intensity of competition in quick commerce made headlines in September 2024 when a man received his iPhone 16 via the quick commerce app Flipkart Minutes while standing in the queue at the Apple store.

All analysts are bullish on Zomato’s quick commerce business Blinkit and expect it to become bigger than the food delivery business. For Zomato to replicate the success of its food delivery business in quick commerce, it has to maintain a market leadership position. And to get more market share, Zomato is getting aggressive with its Blinkit expansion plans.

The race for dark stores

Story continues below this ad

In quick commerce, expansion requires a denser network of dark stores and warehouses with a large assortment of product offerings, from apples to Apple’s iPhone. The denser the network, the faster the delivery attracting more orders. Hence, the race for dark stores is growing.

In Q1FY25, Swiggy’s Instamart had 557 active dark stores across 32 cities, whereas Blinkit had 639 active dark stores across 44 cities. At that time, Blinkit decided to add 2,000 more dark stores in the top 10 cities by December 2026, expanding cautiously.

However, Zomato decided to move aggressively as competition intensified. It spent Rs 370 crore on setting up 368 new dark stores in the last six months, increasing its dark store count to 1,007. It has injected another Rs 500 crore and plans to achieve the 2,000-store count by December 2025 instead of December 2026. The aggressive growth has increased operating expenses and reduced profitability in the short term.

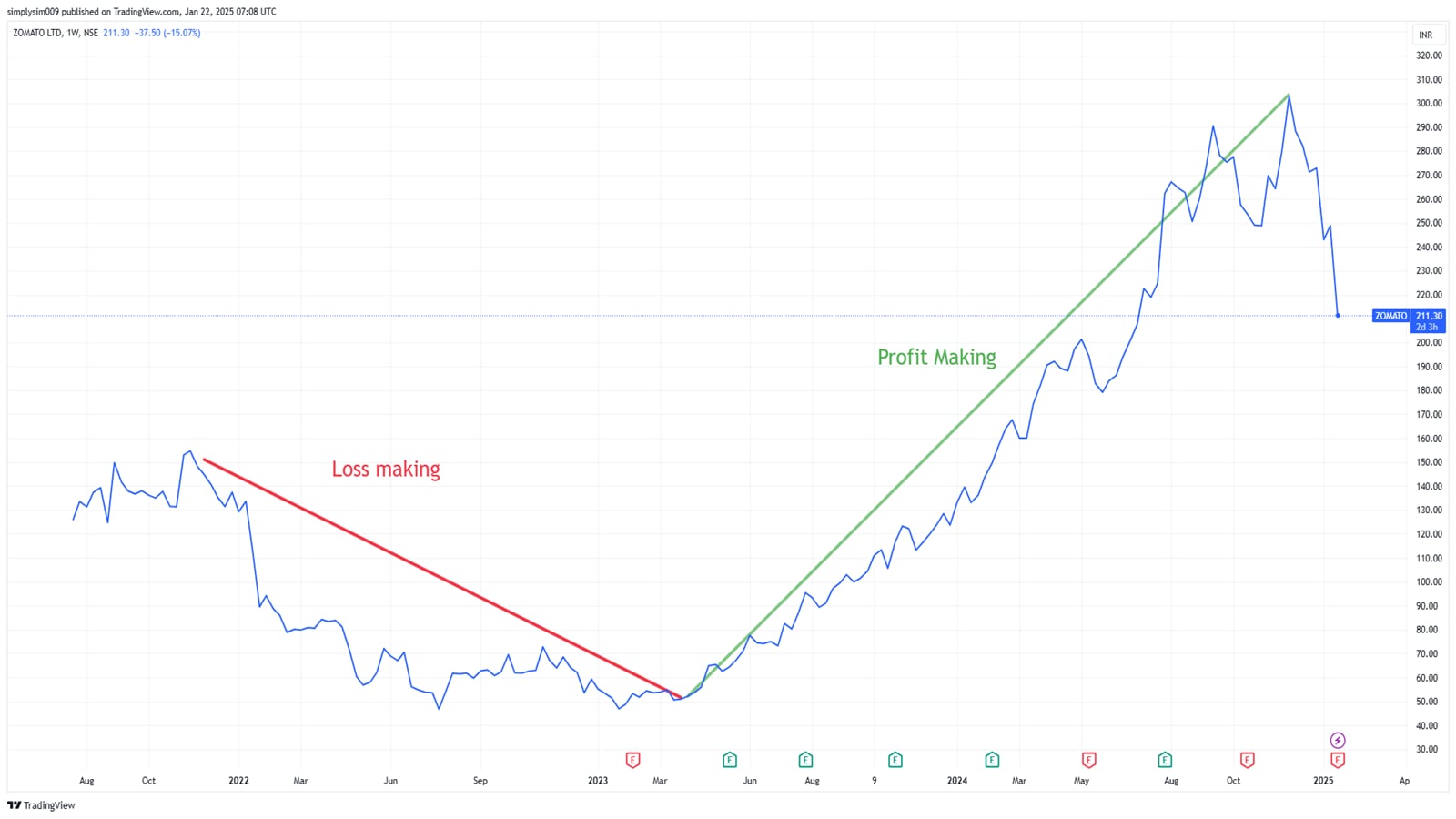

Zomato’s Stock Price Momentum (November 2023 to January 2025)

Zomato’s Stock Price Momentum (November 2023 to January 2025)

Source: Zomato’s Q3FY25 Shareholder’s Letter

Story continues below this ad

Before the aggressive expansion, Blinkit’s Q1FY25 gross order volume (GOV) per store was around ₹10 lakh per day from 639 stores, with the top 50 stores reporting ₹18 lakh per day. However, the company did not provide these stats for the last two quarters. This could be a cause of concern as it could reduce profits in the coming quarters.

However, Zomato prioritised growth over profitability, which is necessary to maintain and grow market share and remain competitive.

Should investors be concerned?

Investors and analysts would keep an eye on Blinkit’s GOV and revenue growth figures. Once the competition stabilises, Zomato could shift its focus to profitability. It could close poor-performing stores that are not contributing enough to GOV to make its quick-commerce network more efficient.

It did so with its food delivery business too. Zomato aggressively expanded its food delivery operations as competition intensified. In January 2023, it closed operations in 225 cities which contributed only 0.3% of its GOV. The act of pruning earned Zomato its first operating profit of Rs 12 crore in the June 2023 quarter (Q1FY24).

Story continues below this ad

If we look at Zomato’s share price trajectory, the operating losses pulled the stock down 30% between November 2022 and March 2023. However, the sound of profits revived investor confidence and the stock began its rally from 1 April 2023, surging as high as 496% till 6 December 2024.

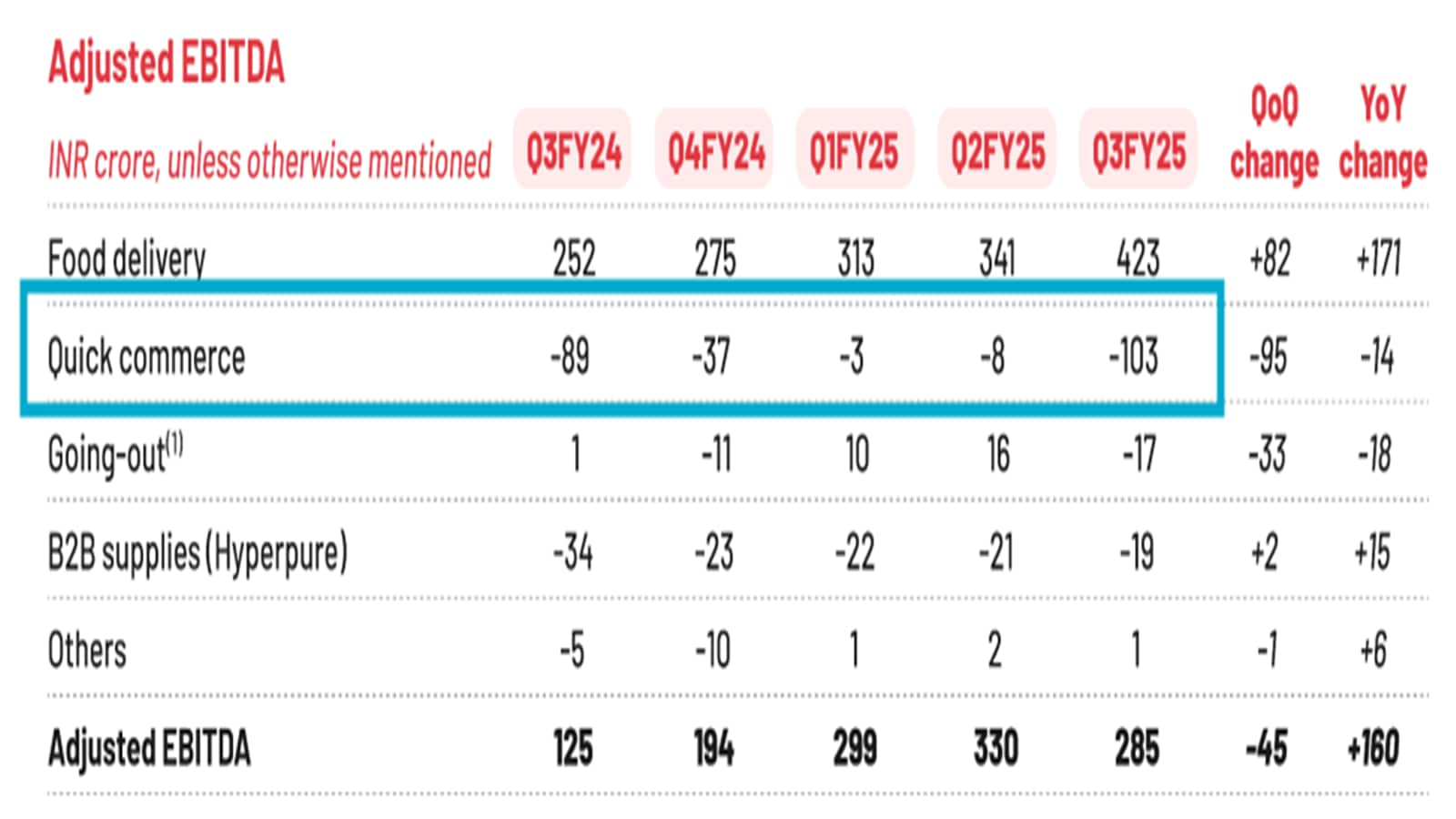

Zomato’s Adjusted EBITDA (Source: Trading view)

Zomato’s Adjusted EBITDA (Source: Trading view)

What do analysts have to say about Zomato’s expansion plans?

Bernstein stated that the dark store expansion strategy is a trade-off between growth and margins. However, it remains bullish on Zomato’s leadership positioning in food delivery and quick commerce. Hence, corrections due to competition concerns are a buying opportunity.

However, Jeffries has cautioned that aggressive competition could lead to heavy discounting and hurt Zomato’s medium-term profitability. It has significantly reduced its profitability estimates for FY26-27.

Story continues below this ad

While the food delivery business remains the cash cow for Zomato, Blinkit is its growth catalyst. There is also Hyperpure business that is growing consistently and is heading towards the road to profitability as the business scales. There is also the going-out business, which Zomato plans to consolidate with the District platform, its venture away from food and into lifestyle services, sports ticketing, live performances, shopping, staycations, etc. The business is still firming its ground and is unlikely to impact Zomato’s share price.

In conclusion

Zomato’s recent stock price correction comes on the back of the company resetting expectations of profitability for some more time. And this strategy of going for growth at the expense of profits is already in play as is indicated by a high PE ratio of over 300x. The stock could dip in the short term as the company may post more profit declines in the coming quarters amid aggressive expansion. However, the long-term growth prospects look bright.

The next growth phase could be tough as the entry of Swiggy in the stock market gives investors a competitor to compare the metrics. So far, Zomato is leading with superior economic units.

And Zepto could apparently be headed for a listing too, giving investors more choice. Not to be left behind is Amazon. Their quick commerce product, Tez, is also starting to roll out.

Story continues below this ad

It would be interesting to see how Zomato executes its quick commerce business expansion. Whether they come through or not for investors remains to be seen. But one thing is for certain. Given the intense competition, the consumer is in for a great run!

Note: We have relied on data from http://www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Puja Tayal is a financial writer with over 17 years of experience in the field of fundamental research.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

Story continues below this ad

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.