Microfinance stocks at historic lows: Signs of a turnaround or more pain ahead? | Smart Stocks News

Before the market-wide correction began in September 2024, the microfinance industry — focused on lending to the ‘bottom of the pyramid’ —was already showing signs of stress. Listed microfinance NBFCs and small finance banks had been grappling with rising NPAs, increased provisioning and write-offs, and declining profits for nearly four quarters. Consequently, stock prices have plunged 40-50% since December 2023.

Between December 2023 and March 2024, a record number of small finance banks and NBFC-MFIs went public, hinting at a likely peak in the cycle. Among the 12 MFI lenders under our coverage (comprising five NBFCs and seven small finance banks), six debuted on the stock exchanges during this period: Muthoot Microfin Ltd, Fusion Finance Ltd, Capital Small Finance Bank, Utkarsh Small Finance Bank, Jana Small Finance Bank, and ESAF Small Finance Bank.

Since listing, these stocks have seen severe price corrections, with many hitting fresh 52-week lows. This downturn raises a key question: Is there an opportunity for value investors?

The risk in bottom fishing

While investing in quality MFIs at low valuations has historically yielded strong returns, the sector remains highly volatile. A key challenge is the instability of book value —the denominator in the widely used price-to-book (P/B) ratio.

Since microfinance, much like most lending businesses, is a ‘leveraged’ business, every Rs 1 of loans that turn bad (not repaid) can impact the equity (book value) of the lender by Rs 3-5.

For example, if equity capital is 25% (Rs 25) of the total loan book of Rs 100, even a 5% NPA would wipe out 20% of equity capital.

In this way, losses (write-offs on account of NPAs) are also multiplied. Historical evidence suggests that industry-wide NPAs of 10-15%+ are not anomalies but recurring features of the sector, making microfinance inherently risky.

Story continues below this ad

Standing between the deterioration of loans and the deterioration of the equity or book value of an MFI player are two lines of defence:

1. Current profitability, which is used to balance against the write-off of bad loans (to the extent possible).

2. Timely capital raises from investors to beef up equity capital. This should be ideally done during the good times, i.e., at higher valuations. These capital raises can buffer against impacts that are not taken care of on the P&L level.

For instance, in Q3FY25, Fusion Finance reported a total income of Rs 482.5 crore but incurred an impairment loss of Rs 573 crore due to rising NPAs (12% as of Q3FY25). This led to a loss of Rs 507 crore, with cumulative losses for 9MFY25 reaching Rs 968.5 crore. Consequently, its equity capital dropped from Rs 2,848 crore at the beginning of FY25 to Rs 1,806.5 crore by Q3FY25.

Story continues below this ad

On December 4, Warburg Pincus-backed Fusion Finance secured board approval to raise Rs 800 crore through a rights issue. Whether investors will participate remains uncertain.

On the other end of the spectrum lies Credit Access Grameen Ltd.

Starting from a book value of Rs 6,570 crore in FY24, it has taken a hit to the P&L of Rs 1,346.6 crore in 9MFY25, yet during the period, its book value rose 5% to Rs 6,906 crore.

This is because in 9MFY25, despite a high impairment hit to the P&L, it earned a profit of about 484 crore. Its impairment as a percentage of the loan book is 5.07% compared to 16.3% for Fusion Finance.

Story continues below this ad

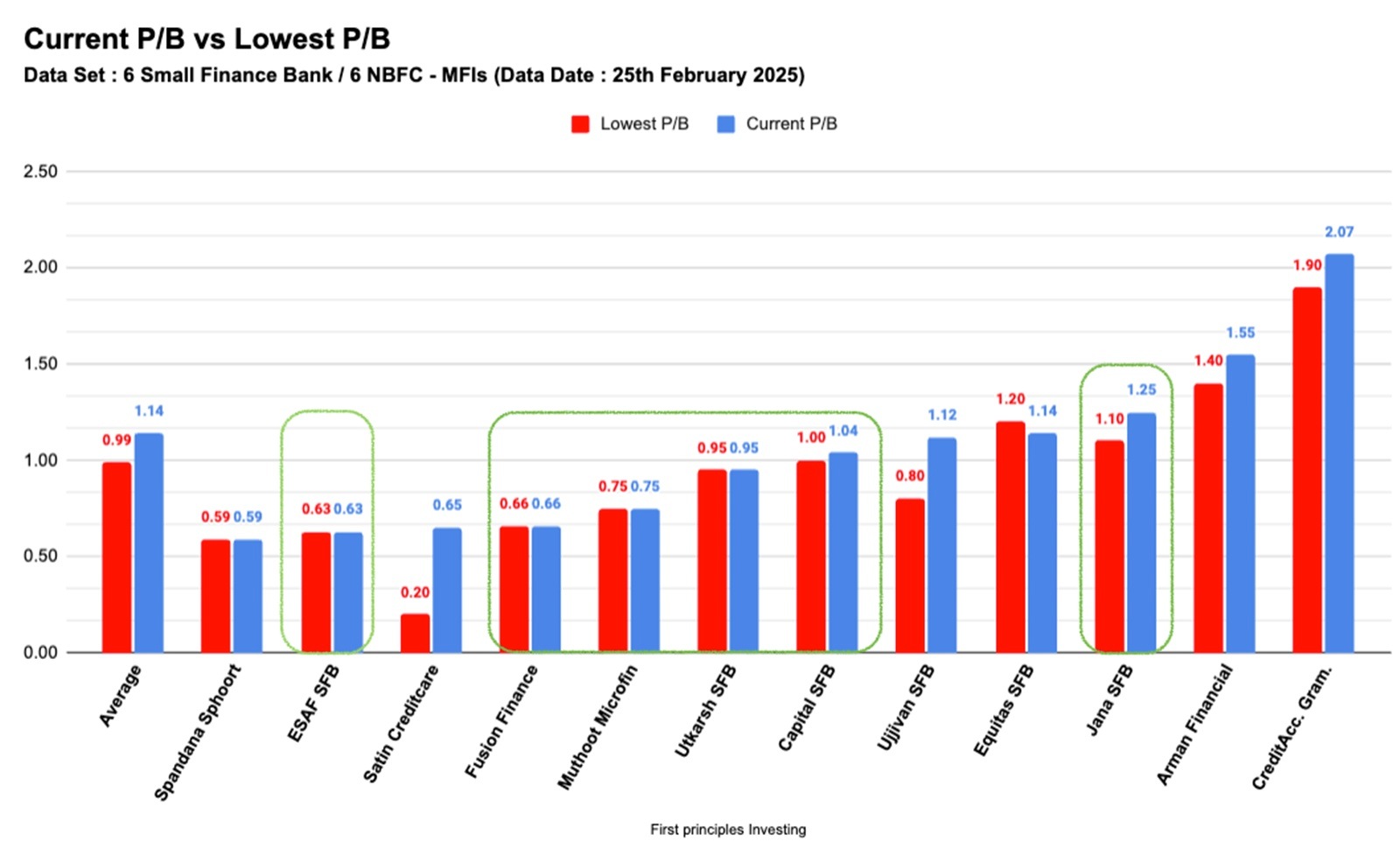

So, when we say that the price-to-book value of microfinance lenders is at an all-time low, it must be remembered that the “book value” can erode further.

Nonetheless, even in an industry fraught with frequently occurring existential threats, some MFIs have continued to navigate these challenges better than others. And Most MFIs are close to or within a few percentage points of their all-time low price-to-book valuations.

Fig 2 (Source: http://www.screener.in)

Fig 2 (Source: http://www.screener.in)

Is the cycle ‘bottoming out’?

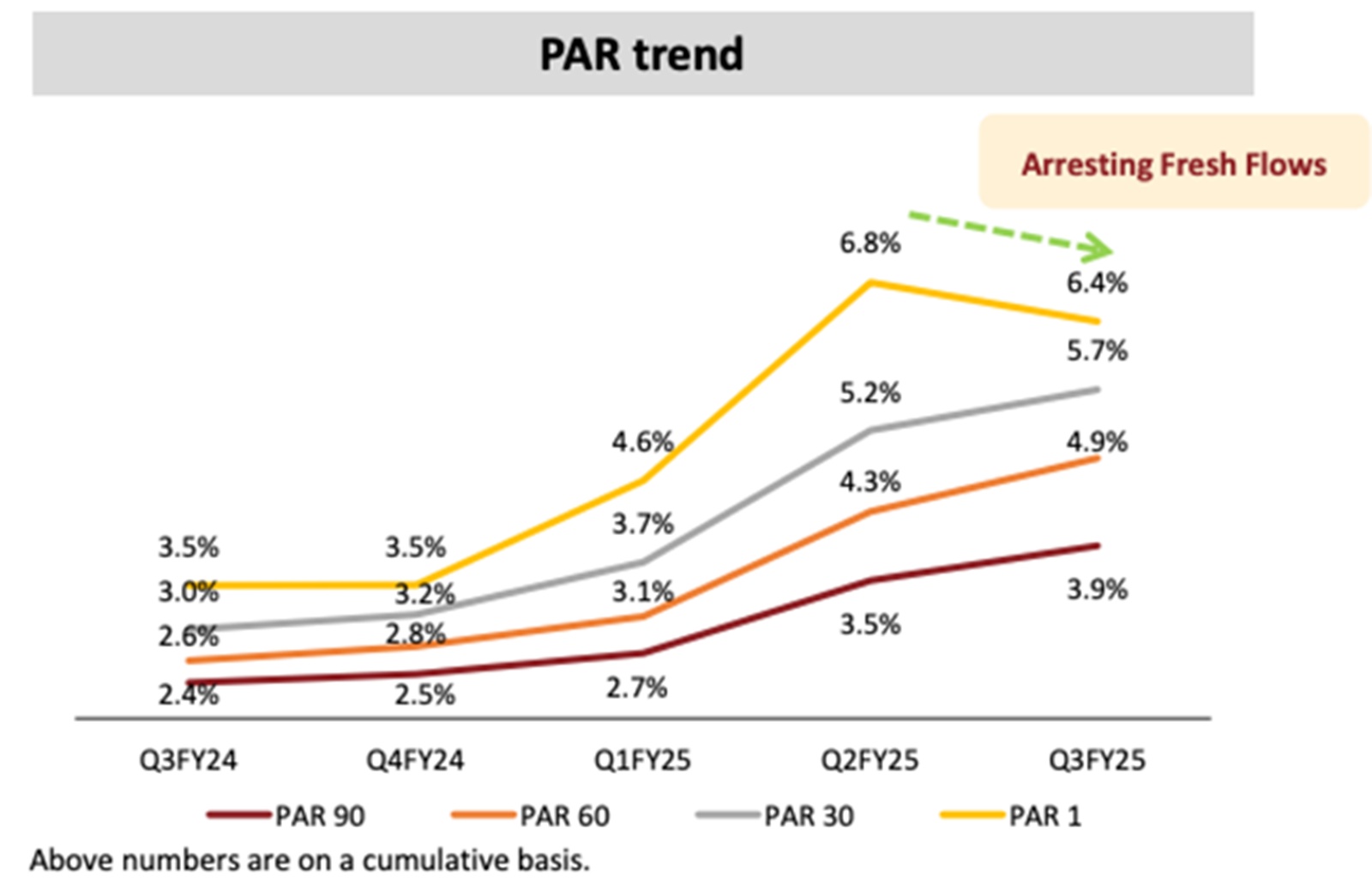

Whether valuations have hit rock bottom depends on asset quality trends. A crucial indicator is the Portfolio at Risk (PAR) accretion rate, which tracks the percentage of loans shifting into NPA buckets.

For example, PAR 15+ means the percentage of loan book that is becoming due by more than 15 days. A trend in the PAR buckets (whether PAR1, PAR15, PAR30) can serve as a lead indicator of whether asset quality is likely to improve.

Story continues below this ad

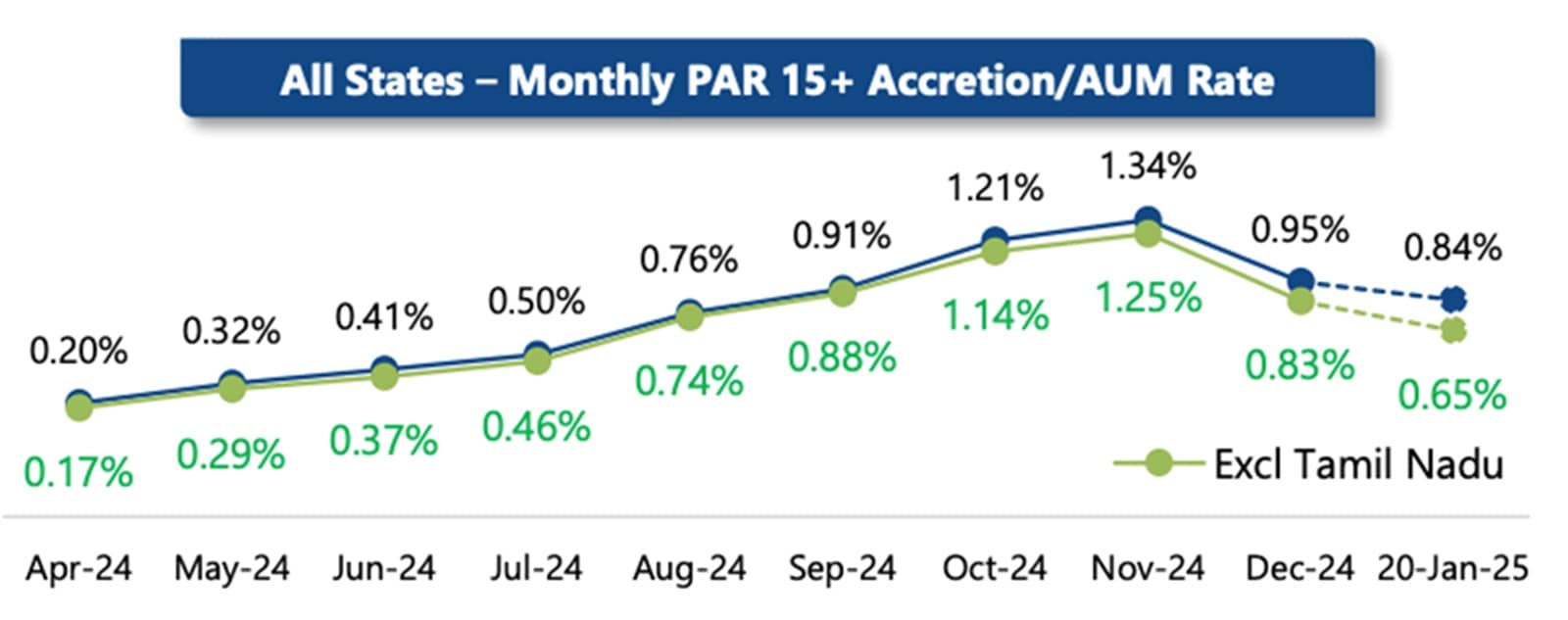

CreditAccessGrameen Ltd (CAG) reported that PAR 15+ accretion rate peaked in November 2024, signaling improving conditions.

Fig 3 (Source: CreditAccessGrameen/Q3FY25 con-call)

Fig 3 (Source: CreditAccessGrameen/Q3FY25 con-call)

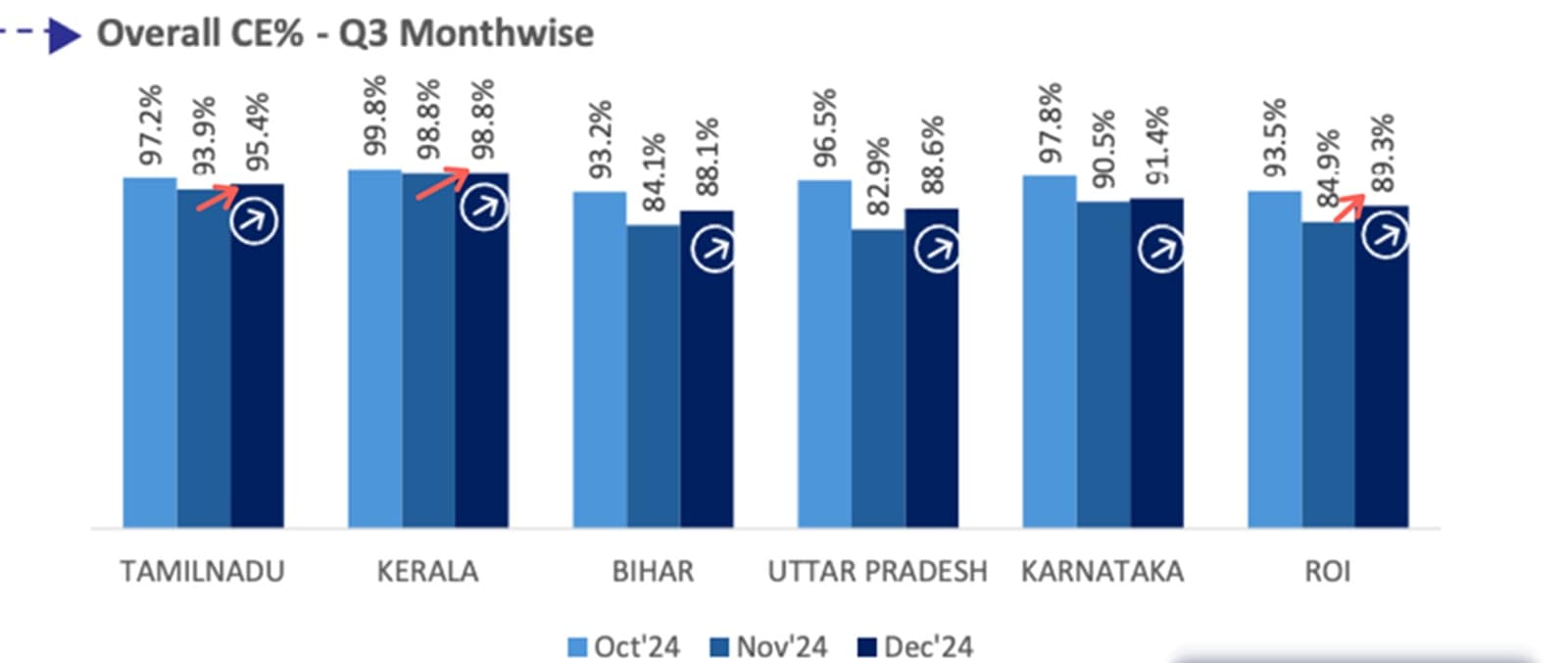

Fig 4 (Source: Muthoot Microfin/Q3FY25 Investor Presentation)

Fig 4 (Source: Muthoot Microfin/Q3FY25 Investor Presentation)

Spandana Spoorthy, with about 27% loan book in East India, in its Q3FY25 management call, said, “In December, we saw 2.2% of flows from the X bucket, which is the current bucket into arrears, which has improved from 3.6% in November. So 3.6% flow has gone down to 2.2%. Any improvement in current book indicates a smaller pool which flows into the subsequent buckets. As this trend solidifies, we expect delinquencies and forward flows to reduce”.

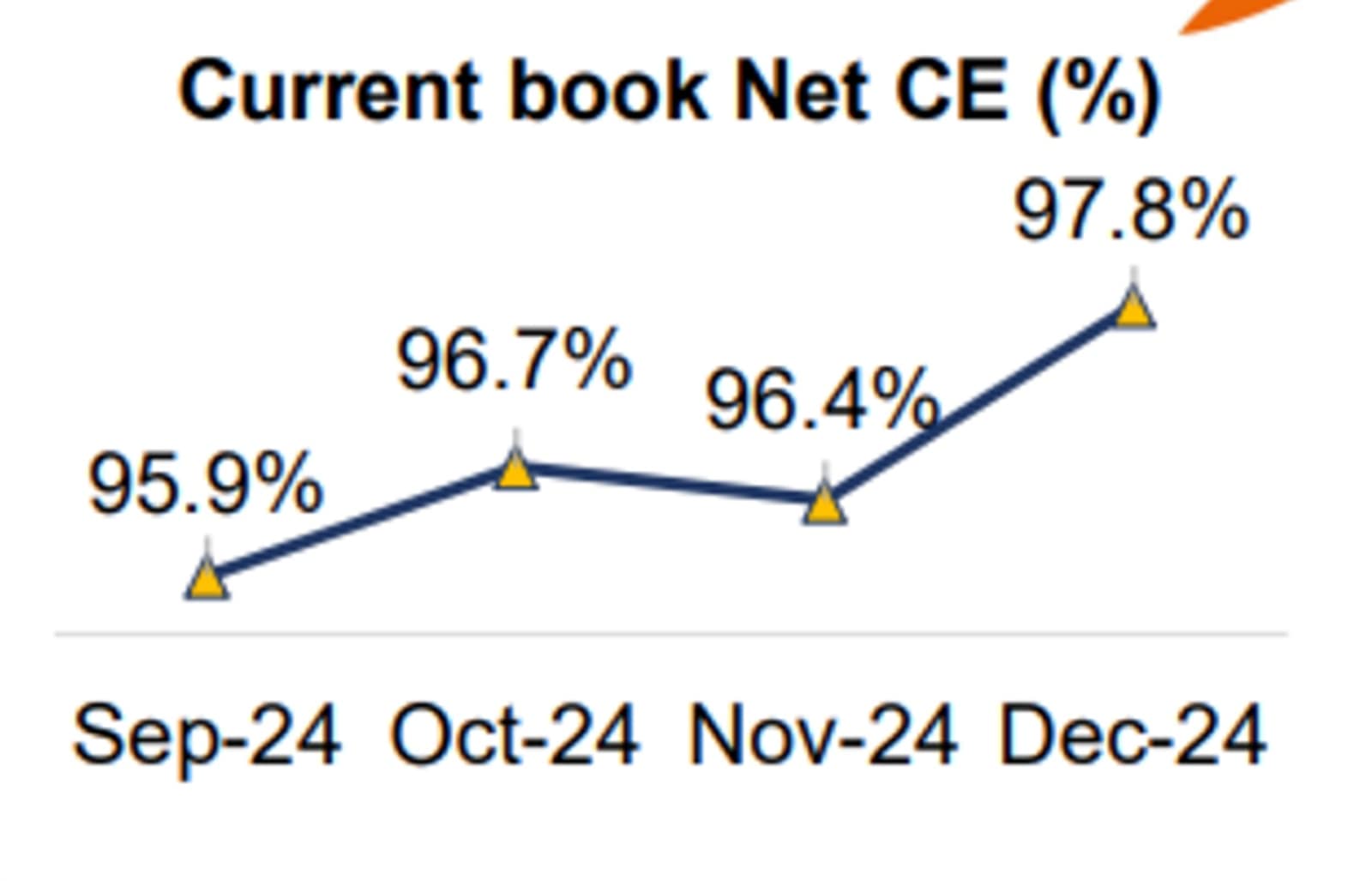

Fig 5 (Source: Spandana Spoorthy/Q3FY25 Investor Presentation)

Fig 5 (Source: Spandana Spoorthy/Q3FY25 Investor Presentation)

Satin Creditcare, which has more than 55% of its loan book in UP, Bihar, Assam, and West Bengal, reported a significant decline in net fresh PAR flow. In its Q3FY25 investor call, it said, “Our portfolio has experienced reversal in delinquency trend…Net fresh PAR flow has seen a significant decline, reducing from 1.61% in October 2024 to 0.45% in January 2025.”

Fig 6 (Source: Satin Creditcare Network/Q3FY25 Investor Presentation)

Fig 6 (Source: Satin Creditcare Network/Q3FY25 Investor Presentation)

Arman Financial, which has nearly 80% of its portfolio in Gujarat, Rajasthan, MP, and UP, reported that “flow forward rates, if it gives a little bit of comfort, are improving at every bucket”.

Story continues below this ad

Fig 7 (Source: Arman Financial Ltd/Q3FY25 Investor Presentation)

Fig 7 (Source: Arman Financial Ltd/Q3FY25 Investor Presentation)

While these data points indicate a potential reversal in asset quality deterioration, it remains uncertain whether this trend is temporary or the start of a sustained recovery.

The road ahead

When the cycle turns, stronger players will be well-positioned to disburse loans faster and grow their profits faster. As weaker MFIs struggle with capital raises and past missteps, better-prepared lenders will seize market share.

The key questions remain: When will the next up-cycle begin, and which MFIs will emerge as winners?

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Story continues below this ad

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer and his dependents hold shares in Arman Financial Ltd.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.