India’s Only 5G Powerhouse is Sitting on a ₹2,363 Crore Inventory Pile—Here’s What’s Stalling the Payoff

Imagine building a next-generation jet engine, proving it works by powering a massive national fleet, and then being told the next batch of orders is “on the way” while you sit on thousands of expensive parts.

That, in essence, is the paradox facing Tejas Networks.

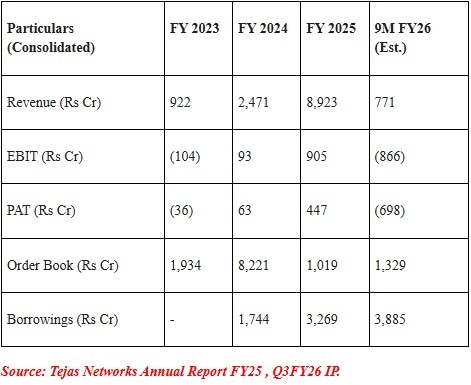

In FY25, the company achieved what many thought impossible: it shipped equipment for nearly 100,000 telecom sites for BSNL within 18 months, pushing revenue past Rs 8,900 crore.

Yet by December 2025, the story had changed dramatically. Quarterly revenue plunged from Rs 1,907 crore in March 2025 to just Rs 307 crore in December 2025.

What explains this sudden reversal? Is Tejas Networks a victim of its own success, or a deep-tech company preparing for its next leap?

To understand this, we need to look at three factors: the company’s large inventory build-up, the high-stakes add-on order from BSNL, and Tejas’s push into international markets with NEC.

The BSNL engine and the Tata DNA

The Tejas story is one of persistence and R&D. Founded in 2000, the company spent two decades operating as a niche wireline player before becoming part of the Tata Group in 2021. This backing transformed its balance sheet and allowed it to win the BSNL 4G/5G rollout contract.

In telecom terms, Tejas began as a wireline infrastructure company, supplying optical transport equipment and data routers that move data across fibre-optic networks.

Story continues below this ad

Source: Tejas Networks Annual Report FY25, Page 28-29

Source: Tejas Networks Annual Report FY25, Page 28-29

Today, Tejas is the only Indian company with a complete, field-proven 4G/5G technology stack. It makes everything from the high-power macro radios on telecom towers to the multi-terabit routers that form the backbone of the network. This is a ‘design-led’ business, with over 65% of its 2,370 employees working in R&D.

But being a deep-tech product company is capital-intensive. Unlike a services company like TCS, Tejas has to build physical hardware. Its revenue profile is also inherently lumpy, depending on order books from telecom players. This is evident from the sharp jump in revenue from FY23-25, followed by a contraction in FY26.

Inventory versus the missing order

The core of the current Tejas story lies in its balance sheet. As of December 2025, the company held Rs 2,363 crore in inventory, nearly double its current firm order book of Rs 1,329 crore.

Why build so much inventory while reporting quarterly losses? The answer is a single APO (Advance Purchase Order). TCS, Tejas’s primary partner, has received an APO for 18,685 additional BSNL sites. Tejas’s share of that order is estimated at roughly Rs 1,526 crore.

Story continues below this ad

However, as of March 2026, the APO has not yet converted into a formal Purchase Order (PO). The delay, according to management, is due to BSNL’s operational readiness and site preparation. While the company waits, the interest costs on the Rs 3,885 crore of borrowings needed to fund this inventory are eating into the P&L.

During the Q2 FY26 call, management faced questions from investors about the path to profitability. COO Arnob Roy said the “inventory will deplete very rapidly once we receive the PO”.

But until that happens, Tejas remains in a high-stakes waiting game.

Forward-looking opportunity: The pivot to private and international

In FY25, BSNL-related shipments through TCS dominated the 94% ‘India Private’ revenue mix. By FY26, the company is trying to diversify.

Story continues below this ad

The real opportunity and risk over the next 12-24 months lies in two areas:

1) The NEC Partnership: On February 26, 2026, Tejas signed a strategic collaboration with NEC Japan for 5G Massive MIMO radios and cores for the global market. This isn’t just about tech; it’s about getting NEC’s global sales team to pitch Tejas products.

NEC’s global network provides Tejas with potential access to Tier-1 telcos in the US and Europe who are currently looking to replace Chinese equipment (Huawei/ZTE) with trusted, non-European alternatives. According to the management, these partnerships open up an addressable market of “upwards of $25 billion to $30 billion globally”.

2) The wireline surge: While wireless is lumpy, the ‘wireline’ (broadband routers) business is seeing steady expansion orders from private telcos like Vodafone Idea and Bharat Net Phase-III.

Story continues below this ad

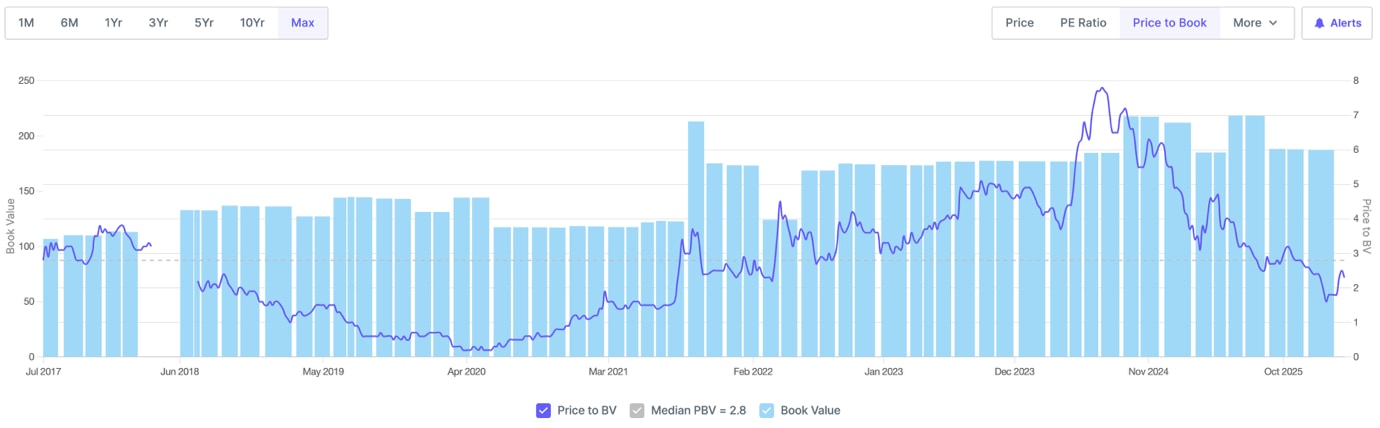

Valuation and outlook

Tejas is not a stock for conservative investors. It is currently valued based on its potential as a global 5G player rather than its current negative earnings. At a consolidated debt level of Rs 3,885 crore and ongoing quarterly losses, the market is pricing in a successful BSNL “add-on” and a meaningful international ramp-up by late 2026.

The bullish view is that the Rs 2,363 crore inventory pile is a “coiled spring”, ready to convert into revenue once BSNL finalises the order.

The bearish argument is that the product company risks, such as the Rs 190 crore obsolescence provision taken in Q2 FY26, suggest that tech moves faster than BSNL’s procurement cycles.

Source: http://www.screener.in

Source: http://www.screener.in

Where does the company go from here? The question is not whether the BSNL order will come, but whether Tejas can fill that revenue gap with international private telcos before the interest costs on its debt become a permanent drag.

Story continues below this ad

The next 12 months will decide if Tejas is the “Ericsson of India” or a R&D-backed turnaround story.

The next 12 months could determine whether Tejas emerges as India’s answer to Ericsson, or is a R&D-backed turnaround story.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He also worked at an AIF, focusing on small and mid-cap opportunities.

Story continues below this ad

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.