Navin Fluorine’s Rs 1,400 crore bet: From refrigerants to oncology and AI cooling | Smart Stocks News

Navin Fluorine International Ltd, once best known for refrigerant gases, is now executing one of the most ambitious transformations in India’s speciality chemicals sector, and the results are beginning to show.

Over the past four quarters, revenue, operating margins and profits have expanded, and the market is recognising this underlying change.

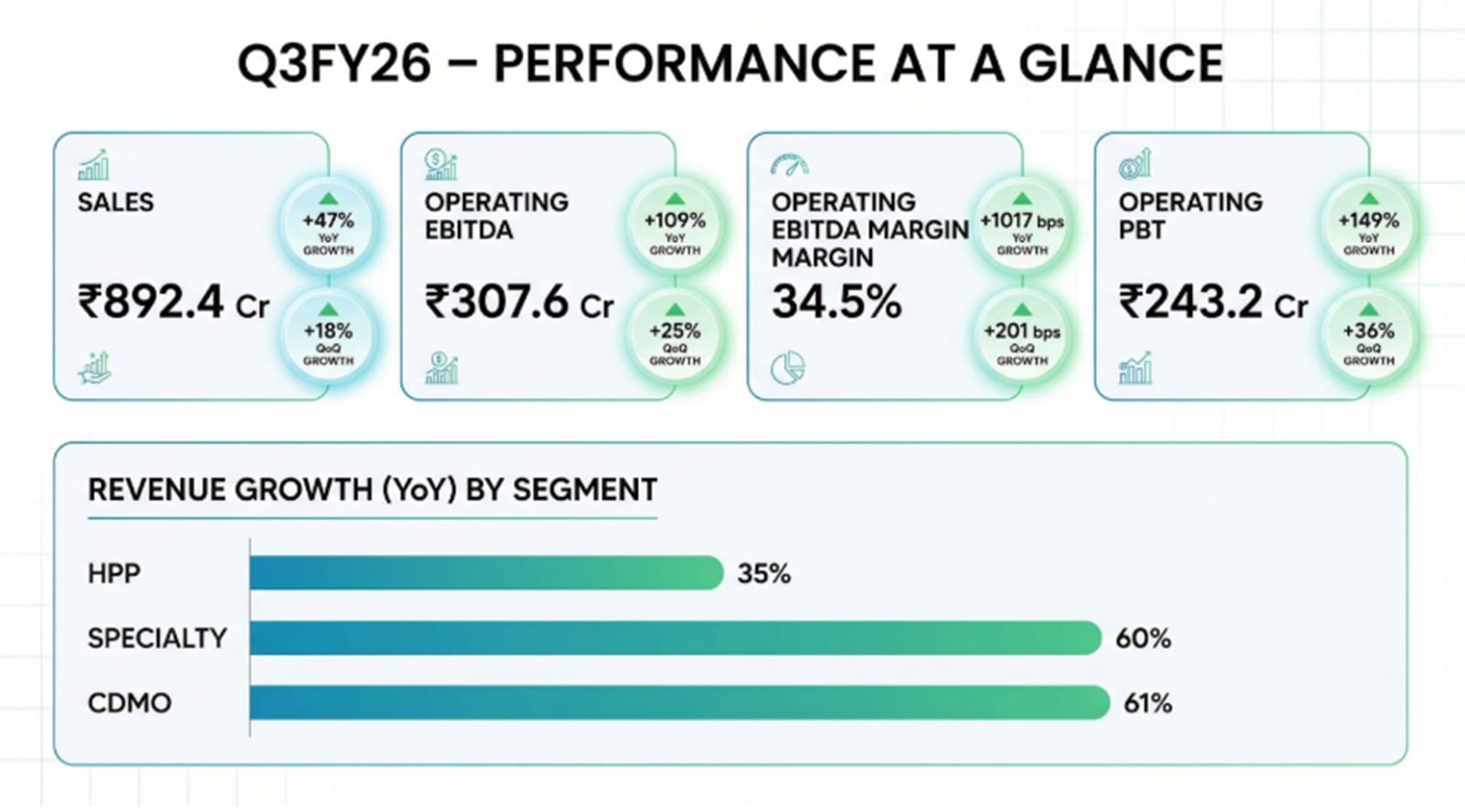

In Q3 FY2026, Navin Fluorine reported EBITDA margins of around 34.5%, higher than its long-term target of 25-30%. Revenue for the current financial year has crossed Rs 2,300 crore, driven by a deliberate shift away from commodity products toward high-margin, custom chemical manufacturing for specific clients.

(Source: Navin Fluorine Ltd Q3FY26 Investor Presentation)

(Source: Navin Fluorine Ltd Q3FY26 Investor Presentation)

At the centre of this transformation is a Rs 1,400 crore capital expenditure programme, the largest in the company’s history. This investment spans backward integration into hydrogen fluoride, next-generation refrigerant capacity, an agrochemical supply deal of global scale, pharmaceutical manufacturing, and a foray into AI data centre cooling.

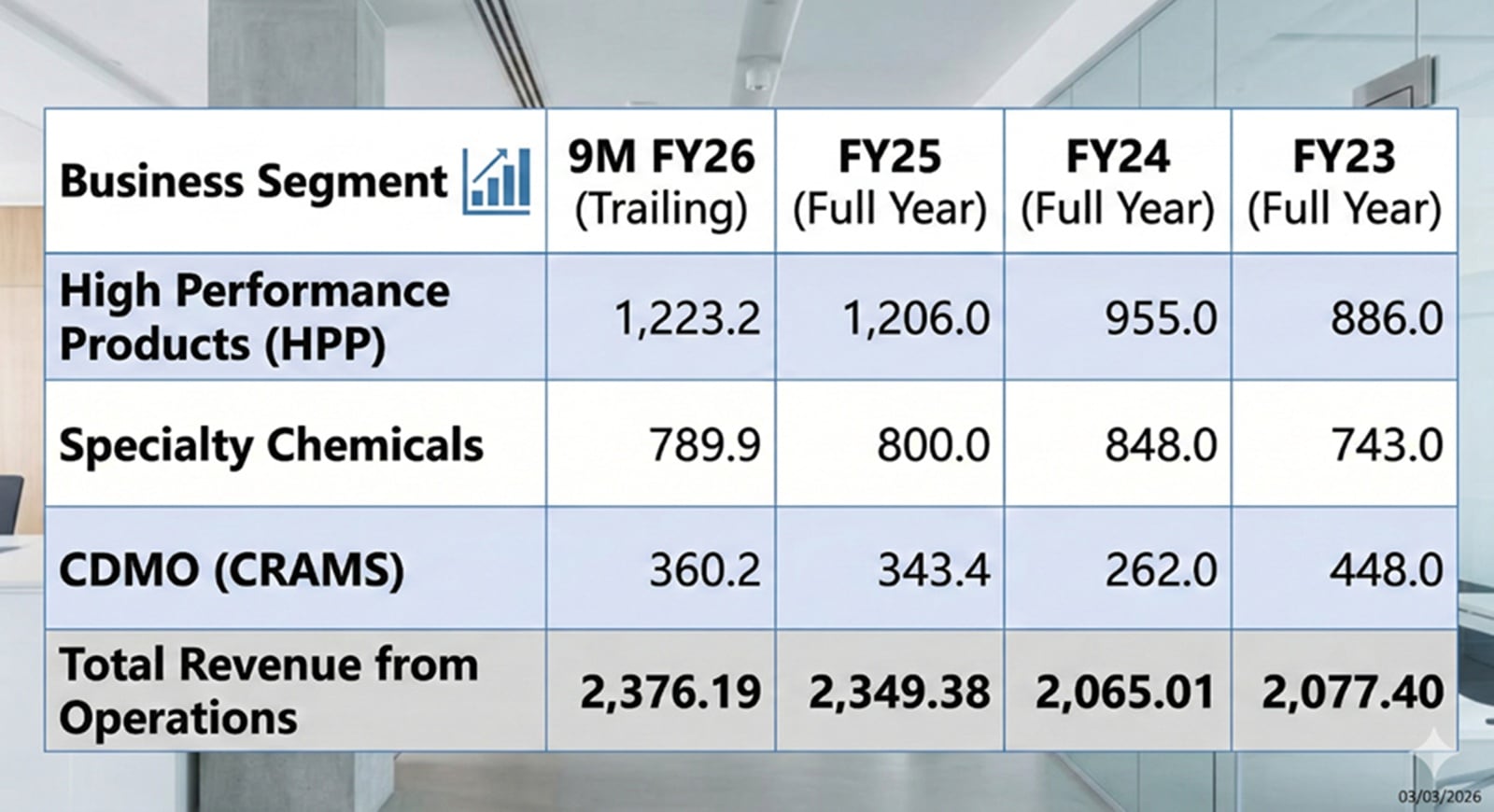

Segmental breakup

Navin Fluorine’s revenue composition has undergone a significant transformation over the last four years.

While legacy products provided the stable cash flows required to fund expansion, the newer segments, particularly CDMO (Contract Development and Manufacturing Organisation) and complex speciality molecules, have become the primary engines of margin expansion.

Story continues below this ad

(Source: Navin Fluorine Ltd Q3FY26 Investor Presentation)

(Source: Navin Fluorine Ltd Q3FY26 Investor Presentation)

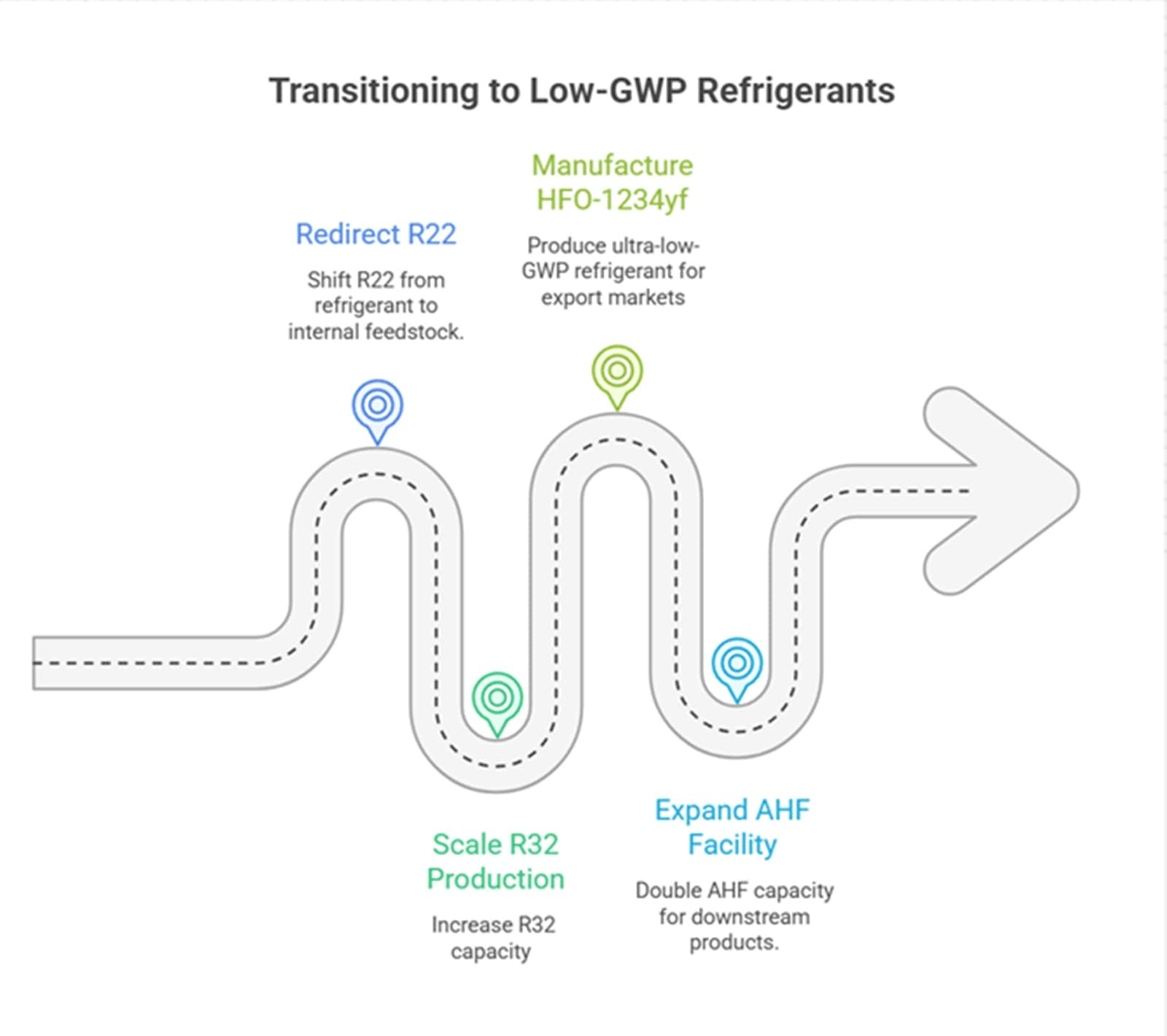

HPP: Betting on the climate transition

The High Performance Products (HPP) segment, which contributes roughly 46-51% of revenue, is undergoing a reinvention. R22, once a flagship refrigerant, is increasingly being used as an internal feedstock as global regulations phase down high-GWP (Global Warming Potential) gases under the Kigali Amendment.

In contrast, R32, a lower-GWP refrigerant that is gaining rapid adoption in residential air conditioning, has emerged as the segment’s growth engine. With India’s AC penetration set to expand sharply through the decade, Navin Fluorine is scaling R32 capacity from 9,000 MTPA to 24,000 MTPA by FY2027.

The company also holds a long-term manufacturing contract with Honeywell for Solstice ® HFO-1234yf(HydroFluoroOlefin), a fourth-generation ultra-low-GWP refrigerant increasingly mandated in passenger vehicles globally.

Navin is the only Indian manufacturer to have the HFO contract with Honeywell.

Story continues below this ad

Supporting this ecosystem is a Rs 450 crore Anhydrous Hydrogen Fluoride (AHF) facility at Dahej, which doubles AHF capacity to 60,000 MTPA. Since hydrogen fluoride is the foundational molecule for virtually all of the company’s downstream products, the investment directly strengthens cost control and supply chain independence.

(Source: Navin Fluorine Ltd Q3FY26 Investor Presentation)

(Source: Navin Fluorine Ltd Q3FY26 Investor Presentation)

Project Nectar: A global agro play

In speciality chemicals, which account for 34-40% of revenue, Navin Fluorine is making a calculated bet on the global agrochemical supply chain’s shift away from China.

Its flagship initiative, Project Nectar, is a Rs 540 crore investment in a fluoro-speciality intermediate facility capable of supplying nearly 50% of global demand for a specific molecule used by a major multinational agrochemical company.

Though ramp-up has been slower than anticipated due to inventory corrections across the global agro sector, management expects utilisation to reach approximately 75% over the next two years.

Story continues below this ad

Data centre cooling: A future optionality

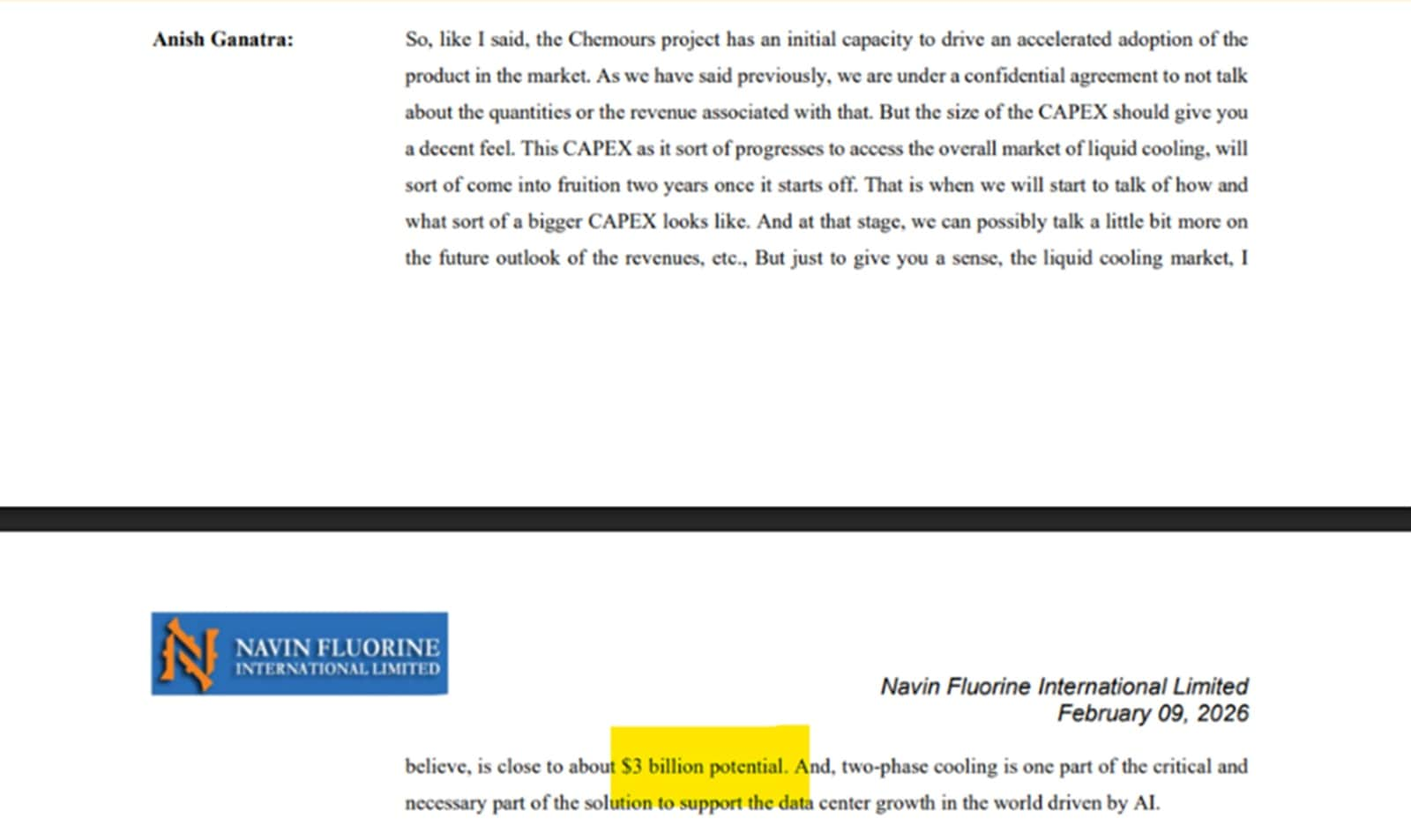

In a less conventional move, Navin Fluorine is entering the data centre cooling space through a partnership with The Chemours Company.

Navin Fluorine will manufacture Opteon™ two-phase immersion cooling fluids, a technology gaining traction in AI data centres where conventional cooling methods are struggling to keep pace with heat-intensive GPU clusters. Commissioning is expected around FY2027.

(Source: Navin Fluorine Ltd Q3FY26 conference call)

(Source: Navin Fluorine Ltd Q3FY26 conference call)

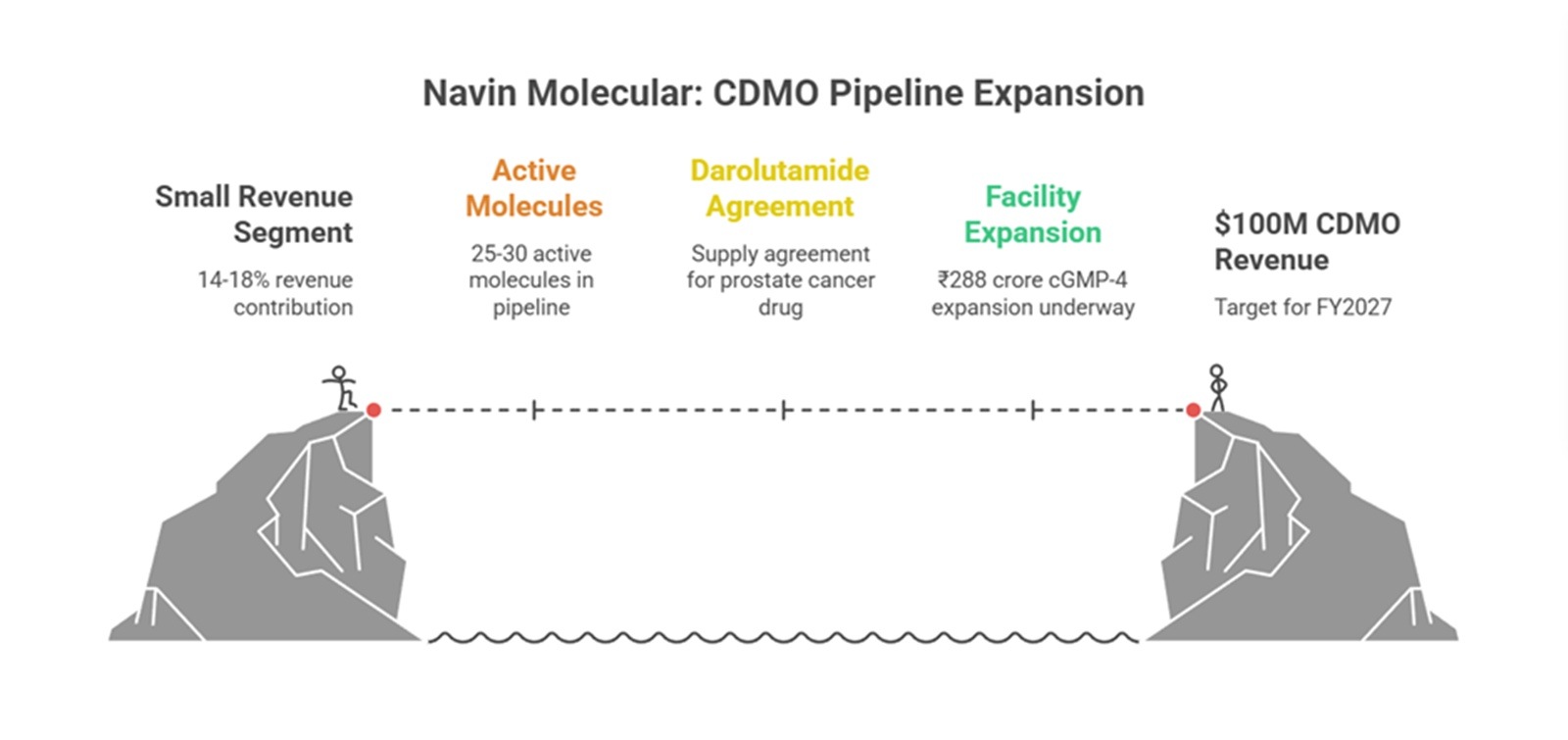

Navin Molecular: The oncology pipeline

The CDMO division, rebranded as Navin Molecular, contributes 14-18% of revenue but is being positioned as the primary driver of future margin expansion.

The pipeline carries 25-30 active molecules, including a commercially significant supply agreement for intermediates used in Darolutamide, marketed as NUBEQA® by Bayer and Orion for advanced prostate cancer. With peak annual sales for the drug now projected at over $3 billion, the relationship provides multi-year revenue visibility.

Story continues below this ad

A Rs 288 crore cGMP-4 (current Good Manufacturing Practice) expansion at its Dewas facility is underway to support long-term Master Service Agreements with global pharmaceutical partners. Management has set a target of $100 million in annual CDMO revenue by FY2027.

(Source: Data from Navin Fluorine Ltd Q3FY26 Investor Presentation)

(Source: Data from Navin Fluorine Ltd Q3FY26 Investor Presentation)

Execution risks remain

Markets have already priced in much of this transformation.

Navin Fluorine trades at an EV/EBITDA multiple of ~33x, compared with 18-25x for most Indian speciality chemical peers. Gujarat Fluorochemicals, a close peer, trades at 25-29x.

This premium reflects expectations of flawless execution across multiple large-scale projects.

That may be optimistic.

Story continues below this ad

Agrochemical cycles remain uncertain. Fluorspar prices are volatile. Project ramp-ups at this scale carry execution risk. And the ongoing capex programme, funded through a combination of internal accruals, moderate debt, and a Rs 750 crore Qualified Institutional Placement completed in 2025, demands consistent utilisation to deliver the return ratios that justify current valuations.

(Source: Data from Navin Fluorine Ltd Q3FY26 Investor Presentation)

(Source: Data from Navin Fluorine Ltd Q3FY26 Investor Presentation)

What is not in question is the strategic logic. Few Indian chemical manufacturers can claim simultaneous exposure to climate-transition refrigerants, China+1 agrochemical supply chains, blockbuster oncology drug intermediates, AI infrastructure materials, and potential semiconductor-grade chemical application – all built on a single, defensible core competency in hazardous fluorination chemistry.

The molecules are in place. The plants are being built. The partnerships are signed.

Whether the next chapter becomes a compounder story or a valuation correction will depend on one thing: execution.

Story continues below this ad

Valuations

At current valuations, the market is not paying for present earnings, it is pricing in a future where Project Nectar is fully ramped up, CDMO revenues approach $100 million, and new-age applications like data centre cooling begin to scale.

(Source: http://www.screener.in)

(Source: http://www.screener.in)

If all of that materialises on schedule, the forward EV/EBITDA may prove justified.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He also worked at an AIF, focusing on small and mid-cap opportunities.

Story continues below this ad

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.