Why China’s 45 MTPA capacity cap is a turning point for NALCO investors | Smart Stocks News

For decades, the world relied on China to bridge gaps in aluminium supply.

Whenever supply gaps emerged, Chinese aluminium was quick to fill the void. From a modest capacity of 4 MTPA in 2004, China’s aluminium capacity surged to 45 MTPA by 2025, accounting for nearly 60% of global aluminium capacity.

On 28 March 2025, China released a new Action Plan (2025-2027) for its aluminium industry.

The key takeaway: capacity has been capped at 45 MTPA.

The plan places strong emphasis on decarbonisation. Measures include benchmarks for green power usage, a ban on smelter operations in high-pollution regions, relocation of older and more polluting smelters to regions with hydro and solar power, and increased use of aluminium scrap to meet demand.

As if this were not disruptive enough for the global aluminium industry, further shocks followed.

In July 2025, the US imposed tariffs on aluminium imports. In addition, the EU is considering measures to restrict exports of aluminium scrap.

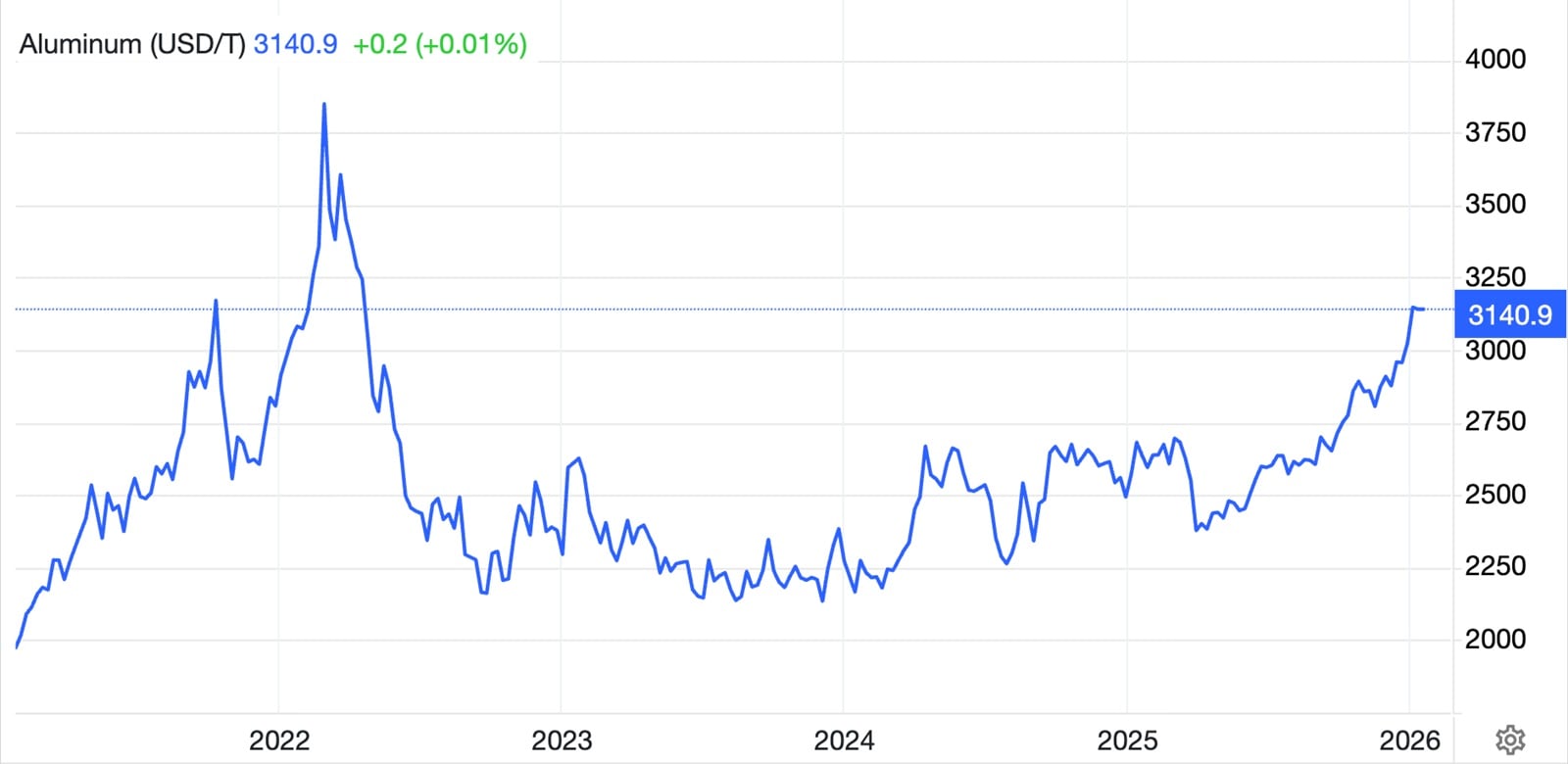

A combination of these factors has sent the global aluminium market into frenzy, pushing prices from $2,300/tonne to $3,140/tonne.

Story continues below this ad

(Source: http://www.tradingeconomics.com)

(Source: http://www.tradingeconomics.com)

In this backdrop, aluminium smelters NALCO, Hindalco, and Vedanta Ltd have benefited. NALCO, in particular, has enjoyed a dream run, but can it sustain this momentum?

(Source: http://www.tradingview.com)

(Source: http://www.tradingview.com)

NALCO: Position in the value chain

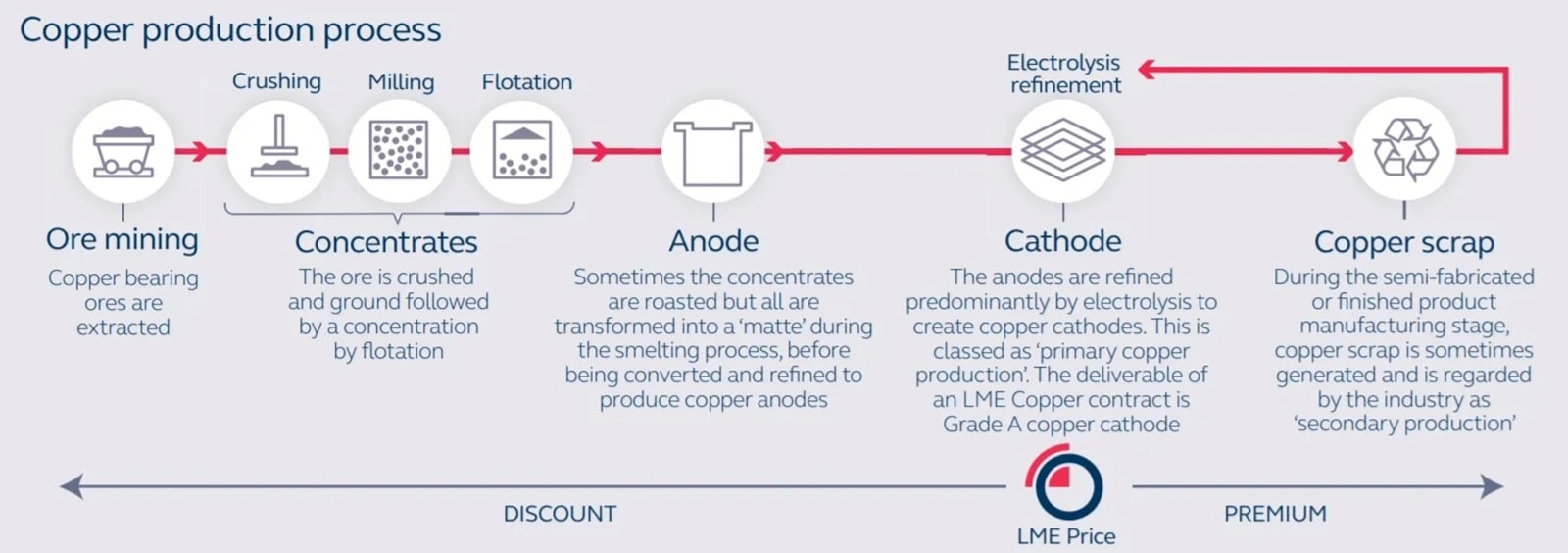

The aluminium value chain comprises three stages: mining bauxite ore, bauxite ore to aluminium oxide (powder) or alumina, and alumina to aluminium smelting.

Copper production process. (Source: http://www.LME.com)

Copper production process. (Source: http://www.LME.com)

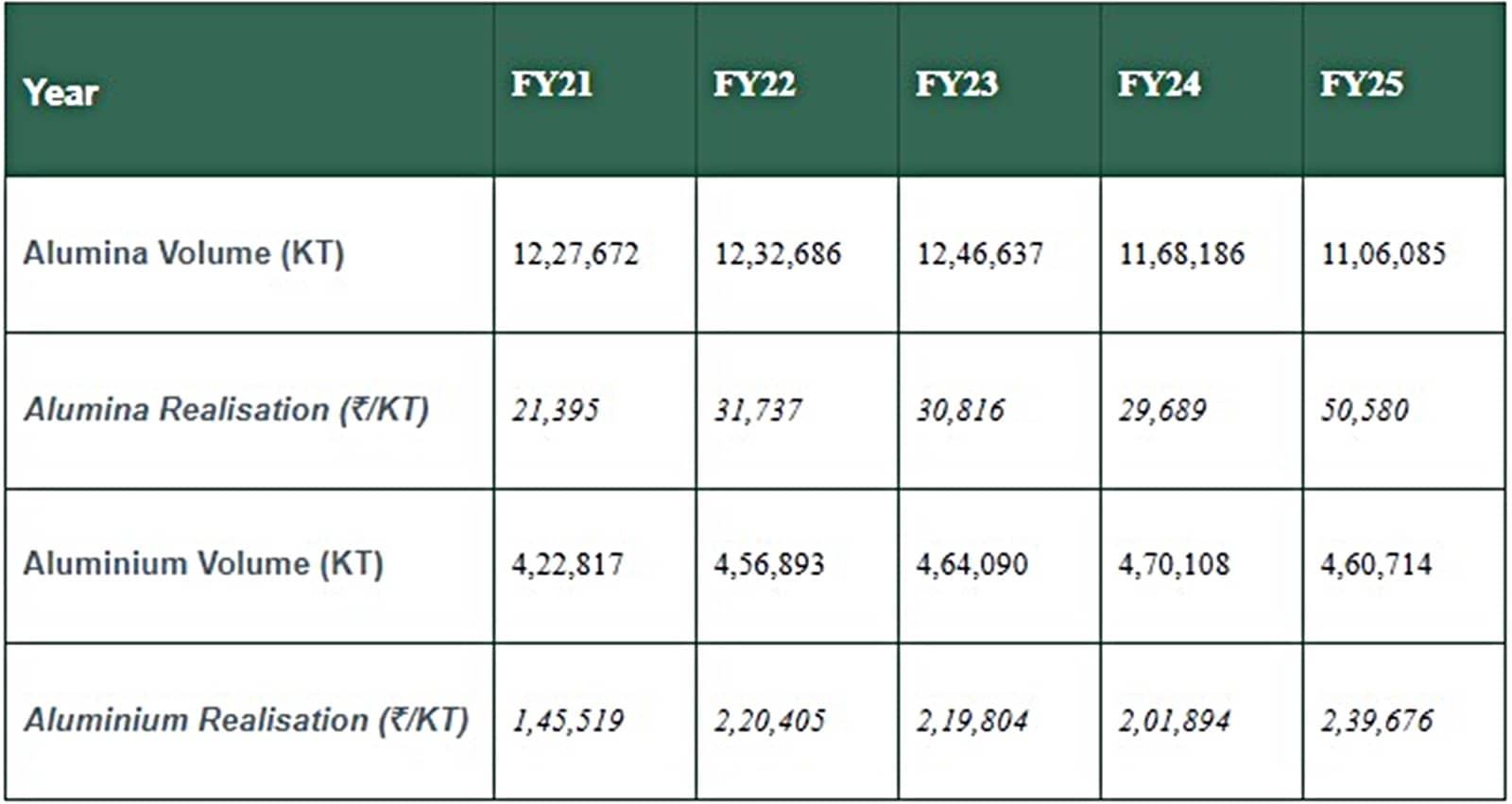

In FY25, NALCO accounted for nearly 25% of India’s alumina refinery capacity. However, its share in the total aluminium metal production is significantly lower, at around 11%.

(Source: Company filings)

(Source: Company filings)

Of NALCO’s 2.3 MTPA alumina production, about 1 MTPA is for internal use (to smelt aluminium metal). The remaining quantity is exported.

Story continues below this ad

Thanks to its proximity to raw materials, NALCO has emerged as one of the lowest-cost producers of alumina in the world.

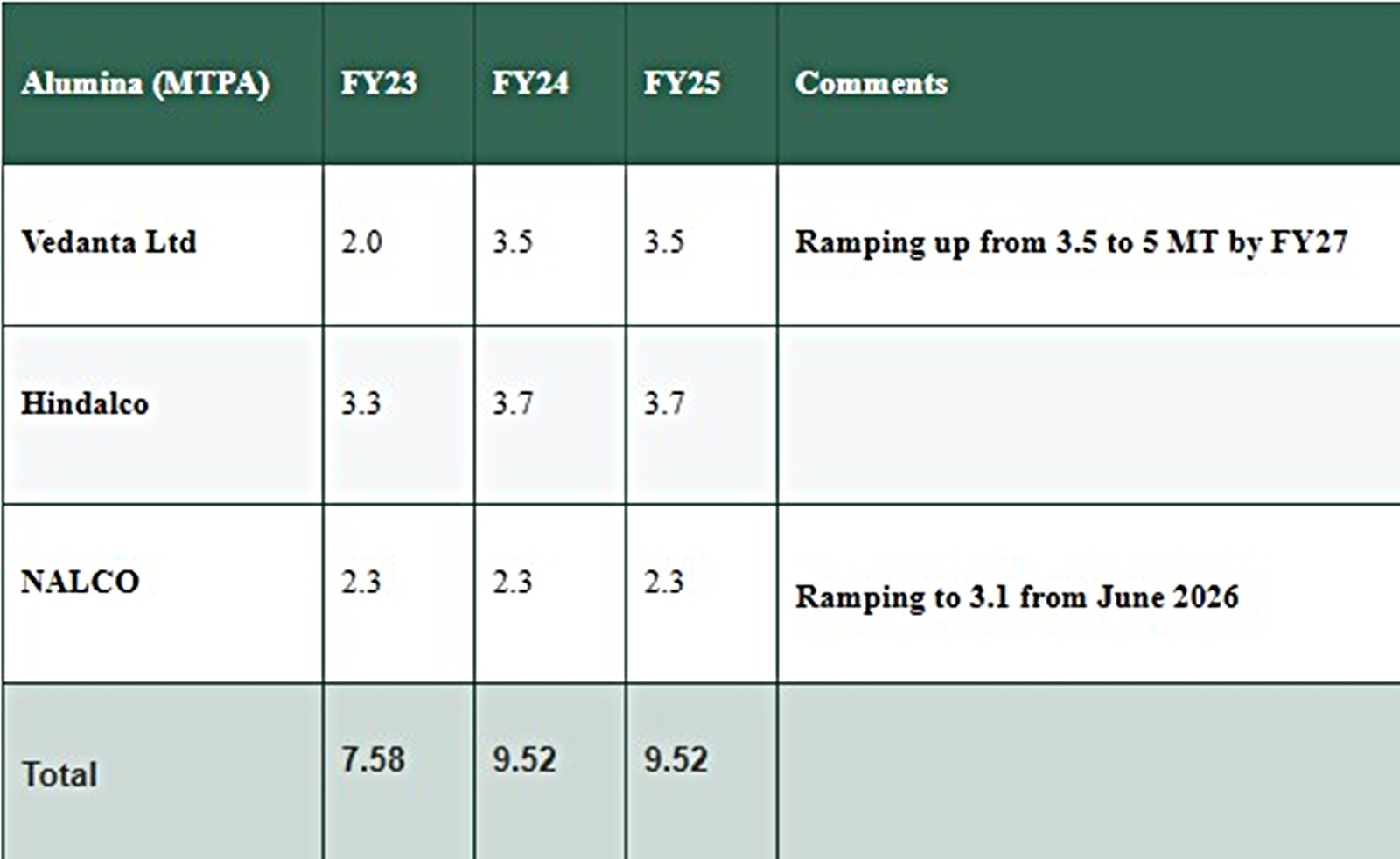

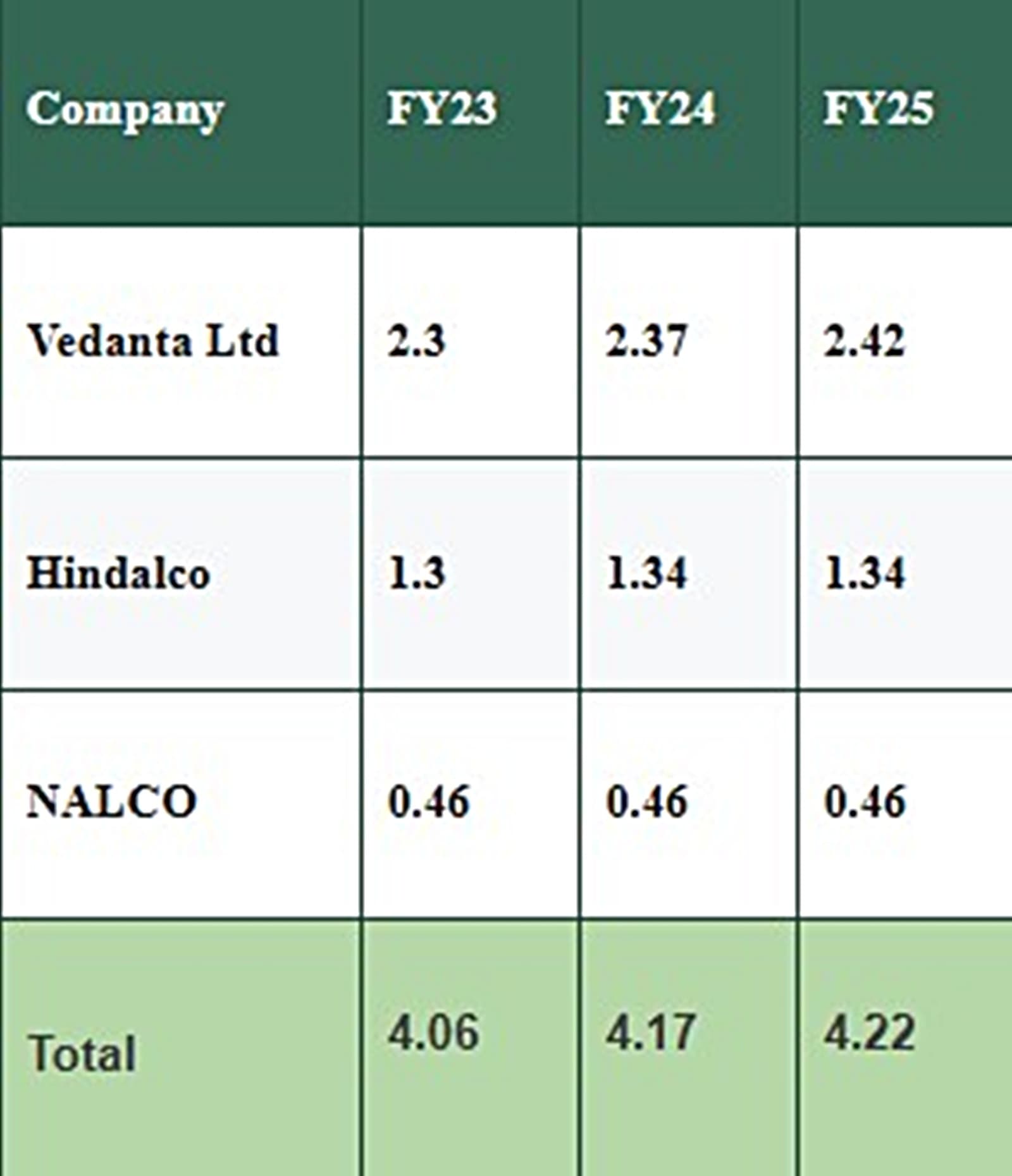

Over the last 10 years, while alumina capacity has increased, NALCO’s smelting capacity has remained stagnant at 0.46 MTPA. Meanwhile, Vedanta has been consistently increasing capacity and is the market leader with 2.42 MTPA, which is set to increase to 3.1MTPA by FY27.

(Source: Company filings)

(Source: Company filings)

However, NALCO has consistently increased its capacity utilisation from 80% in FY2015 to 100% today. Higher utilisation has led to increased revenues, which, along with improving alumina and aluminium prices over the last six months, have led to a sharp improvement in business numbers.

The company has also announced plans to increase smelting capacity by 0.5 MTPA by 2030.

Story continues below this ad

Financial analysis

NALCO’s revenues are primarily driven by sales of alumina and aluminium metal.

(Source: NALCO Company Filings)

(Source: NALCO Company Filings)

Between FY21 and FY25, revenue nearly doubled from Rs 8,900 crore to Rs 16,700 crore, driven largely by higher alumina and aluminium metal pricing. This trend was especially pronounced between FY24 and FY25 because of a sharp increase in realisations in both key products.

Value versus volume

Revenue is a function of value and volume growth.

The company has more control over volume than value. Since there has been zero volume growth in alumina and a marginal increase in metal production on the back of higher utilisation, investors must view this improvement with caution.

Story continues below this ad

Here’s why: The pricing of both products is market-driven, over which the company has zero control. Therefore, volume growth and higher utilisation are more reflective of management quality and prospective future growth.

Since utilisation has consistently improved over the last five years to nearly 100%, where does the company go from here?

Capex plans

NALCO is expanding its alumina refining capacity, with a fifth alumina stream expected to be operational by June 2026. This will add 1 MTPA, taking the total capacity to 3.1 MTPA.

To support this expansion, the company is developing the Pottangi bauxite mine (3.5 MTPA), expected to come online around April 2026.

Story continues below this ad

Given the energy-intensive nature of aluminium smelting, NALCO has also commissioned a new coal mine with a peak capacity of 4 MTPA. This is expected to reduce costs, as coal can be sourced at a discount of Rs 300-400 per tonne versus market rates from Coal India.

The company also plans to expand aluminium smelting capacity by 0.4 MTPA, which is expected to be operational by FY30.

(Source: NALCO, Q2FY26 filings)

(Source: NALCO, Q2FY26 filings)

PAT growth levers

Medium-term growth levers include:

- Alumina 1 MTPA expansion

- Energy cost reduction (Higher coal sourcing from captive Utkal mines)

Pricing remains uncertain for both alumina and aluminium metal.

Story continues below this ad

However, at an average alumina realisation of approximately Rs 30,000 per tonne (three-year average), the incremental 1 MTPA capacity could generate ~Rs 3,000 crore in additional revenue.

For context, that’s about 18% growth on total FY25 revenue of Rs 16,700 crore.

In the aluminium metal, the larger revenue segment, volume growth is not expected until FY30, and pricing remains volatile.

If aluminium prices stabilise around FY25 levels (below the current price of $3140/tonne) and alumina expansion ramps up as planned, the bottom line could improve at a faster rate due to rising captive coal usage from Utkal Block D & E mines.

Under this scenario, PAT growth of 20% appears plausible.

Story continues below this ad

Disclaimer: This is the author’s opinion. Actual outcomes may vary based on multiple factors.

Valuations

The market is currently in the midst of a metals rally. Aluminium prices have shot up on the back of China’s decision to cap aluminium capacity at 45 MTPA.

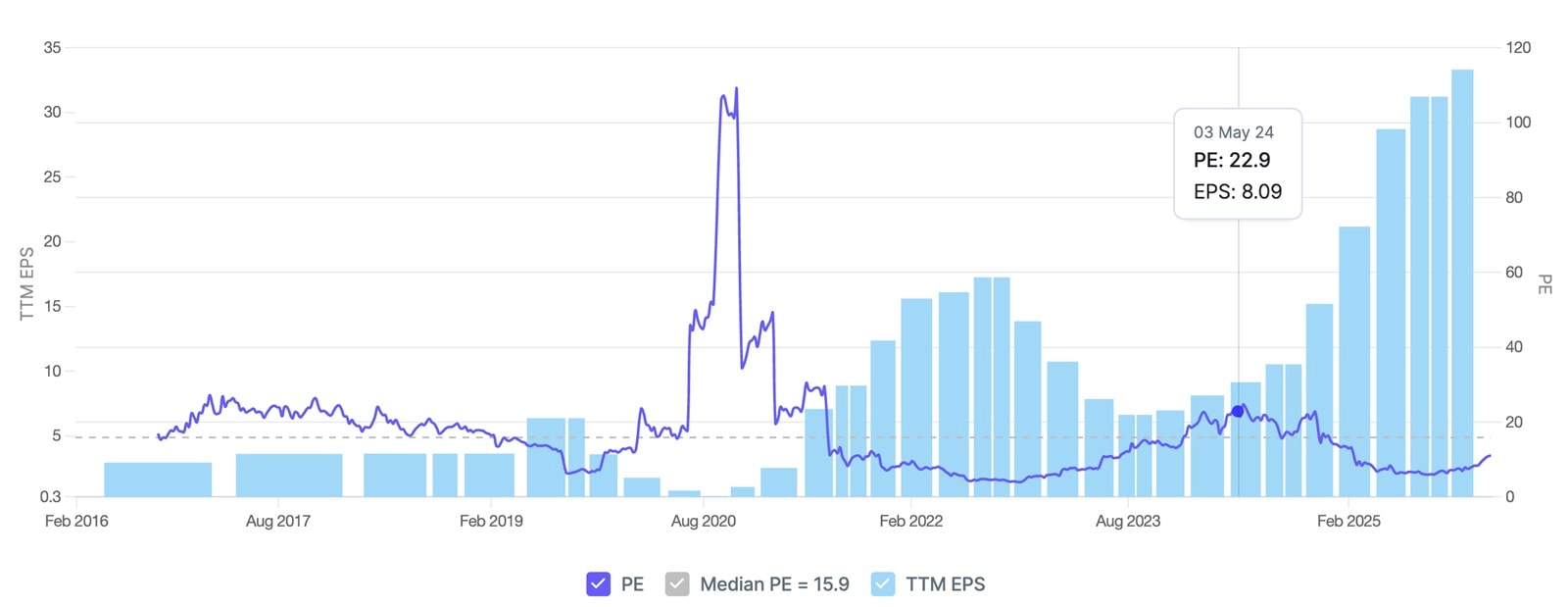

NALCO’s valuations are above the median. Price-to-book is the highest it has ever been.

(Source: http://www.screener.in)

(Source: http://www.screener.in)

For cyclical commodity companies like NALCO, P/E ratios typically move inversely with the cycle. It’s best to enter when PE ratios are high/above median and vice-versa.

At current levels, NALCO does not appear to be a value buy.

(Source: http://www.screener.in)

(Source: http://www.screener.in)

NALCO’s operating performance has materially improved, and it has been discounted to a fair degree. Going forward, business performance and consequently stock price will be contingent on timely alumina production ramp-up and stable alumina and aluminium prices.

While commodity pricing remains unpredictable, China’s policy stance could keep aluminium prices structurally elevated.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.