Why a household favourite has been a stock market laggard for a decade

Step into any Indian home and you will likely find Emami’s products within reach: a jar of BoroPlus in the medicine cabinet, a bottle of Navratna oil on the dressing table, a tube of Zandu balm tucked away for quick relief.

Few FMCG companies have achieved this level of everyday presence across urban apartments and rural households alike. For half a century, Emami has built not just brands but rituals of use that cut across age and region.

Yet for investors, the story looks very different.

A portfolio this entrenched should, in theory, deliver steady compounding and market-beating returns. Instead, Emami’s stock has spent much of the last ten years moving sideways.

The products continue to command loyalty, but the business behind them has struggled to translate that trust into consistent growth. Categories like talc and male grooming have hit natural limits, while newer launches have yet to find the same scale.

This paradox of consumer ubiquity but investor disappointment is what makes Emami’s journey worth examining. As the company celebrates fifty years of brand building, the question shifts from recognition to reward: will the next decade be different for its shareholders?

Stock Price Movement of Emami Ltd. (Source: Screener.in)

Stock Price Movement of Emami Ltd. (Source: Screener.in)

Business model and margins: making sense of the numbers

Emami’s latest results show a familiar pattern. Sales are not racing ahead, but the company still manages to deliver healthy profits.

Story continues below this ad

To understand why, it helps to look at how its business model works and how the margins are being protected.

A brand-led model that keeps costs light

At the heart of Emami’s model are its brands, including Navratna, BoroPlus, Zandu, and Kesh King. Because these products are developed and marketed in-house, the company does not pay outsiders for brand rights or royalties. Most of its ingredients, like menthol, camphor, and herbs, are also relatively low-cost compared to premium cosmetics or detergent chemicals.

This combination gives Emami a natural cushion: its gross margin in Q1 FY26 stood at nearly 70 percent, among the highest in the FMCG space.

High gross margins allow Emami to spend more on advertising than its peers while still keeping money left over. But having a cushion does not automatically solve the growth problem. That is why the next step is to see what happened in the latest quarter.

Story continues below this ad

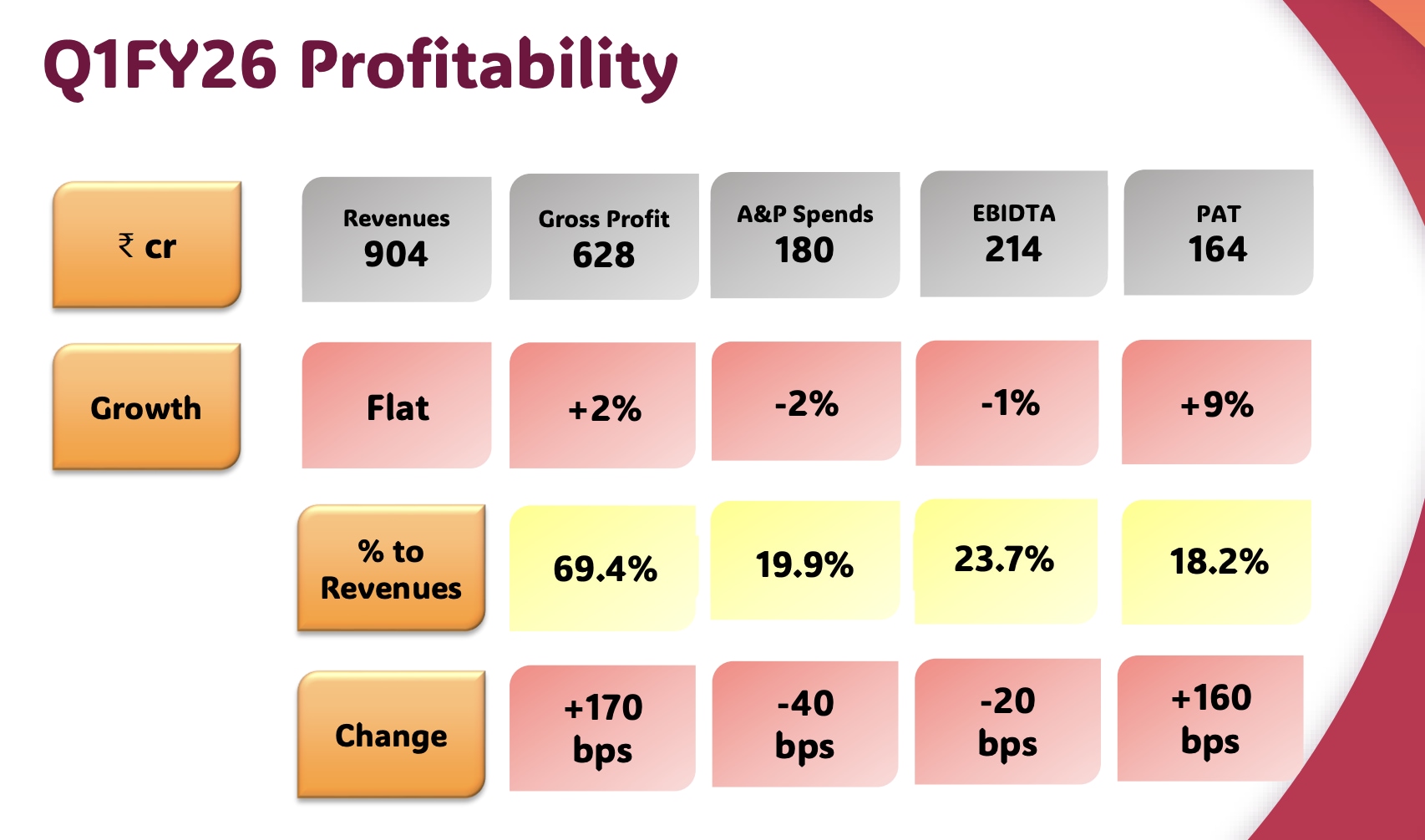

Emami’s Q1FY26 Numbers. (Source: Quarterly Report)

Emami’s Q1FY26 Numbers. (Source: Quarterly Report)

Flat sales but higher profit

On paper, sales were unchanged at Rs 904 crore. Usually, that would mean profits also stay flat. Yet Emami reported a 9 percent increase in net profit, reaching Rs 164 crore.

The answer lies in the sales mix.

The talc and prickly heat portfolio, which is lower margin, dropped 17 percent after a weak summer. At the same time, higher-margin categories such as balms and BoroPlus creams grew strongly. This shift in balance lifted overall margins. Add in lower input costs and a small cut in advertising spend, and profits rose even without top-line growth.

So the model shows its strength: even when demand is uneven, Emami can still protect earnings.

Story continues below this ad

But this raises the next question: how sustainable is this cost-driven profit growth?

Where the money is spent

Every Rs 100 of sales in this quarter breaks down roughly like this: Rs 31 for raw materials, Rs 20 for advertising, Rs 13 for salaries, and another Rs 13 for administration. That leaves Rs 24 as operating profit.

This profile tells two stories.

First, the company is disciplined in controlling costs.

Second, advertising remains a heavy line item at nearly one-fifth of revenue. That spend is not optional, because without constant advertising and brand refresh, categories like male grooming or hair oil risk losing relevance. This means there is limited room to cut further.

To keep profits moving, Emami will need stronger sales, not just tighter belts.

The push into new channels

Story continues below this ad

One way the company is trying to revive sales is by moving into modern trade, e-commerce, and quick commerce.

Quick commerce in particular grew almost three times compared to last year. This helps with reach and visibility, but it also brings new pressures. Modern trade and instant delivery platforms usually demand higher discounts, which can eat into margins if not managed carefully.

This is where investors need to watch closely. Emami has shown it can manage costs well in its traditional business. Whether it can maintain similar margins while expanding into new formats will be a key test.

The nature of profit growth

It is also worth noting that part of the net profit increase came from items below operations.

Story continues below this ad

Other income more than doubled, and tax outgo was lower. These helped lift PAT even though operating profit (EBITDA) was slightly lower than last year. That is not necessarily negative, but it reminds us that true long-term earnings power depends on sales growth, not one-off gains or tax benefits.

What management is thinking

Listening to management after the Q1 FY26 results, a few themes stand out. The leadership knows that the biggest weakness today is not profitability but the lack of steady sales growth.

Their strategy is therefore focused on three levers:

1. Reviving core brands

Emami is working on relaunches and refreshes. Kesh King, the Ayurvedic hair oil acquired a decade ago, is being rebranded with new packaging, pricing, and campaigns. Smart and Handsome (earlier Fair and Handsome) is being expanded into male grooming categories beyond creams, with plans for 10-12 new products this year.

The management admits the fairness cream market has lost relevance and sees diversification as the only way to keep the brand alive.

2. Pushing digital-first brands

Story continues below this ad

The Man Company, in which Emami has a majority stake, returned to growth in June 2025 after a long period of struggle. Management says it is now repositioning the brand with sharper communication and a wider portfolio.

At the same time, the Zanducare platform is being used to launch new Ayurvedic products directly to consumers online. The aim is to capture younger, urban buyers who may not pick up these products at a kirana store.

3. Expanding distribution reach

Modern trade, e-commerce, and especially quick commerce are being treated as high-priority channels. Quick commerce sales were nearly three times higher than last year, and management believes this validates their omnichannel approach.

Rural expansion is also a focus, with vans and promotions being used to deepen reach in smaller towns.

Story continues below this ad

Overall, management remains optimistic. They expect a good monsoon, easing inflation, and stronger consumer sentiment to lift demand in the second half of FY26.

Their message to investors is clear: margins are safe, but sales growth will take a few more quarters to show consistent traction.

How the market values Emami

For investors, the obvious question is whether the stock already reflects this cautious outlook.

Emami currently trades at a price-to-earnings multiple of around 35 times, lower than larger FMCG peers like Hindustan Unilever or Dabur, which trade at 50 times or higher.

The market is giving Emami credit for its strong margins and high return on equity (over 30 percent in recent years ), but it is also discounting it for weak revenue growth.

Over the last 10 years, shareholders have seen limited wealth creation. The stock has had bursts of activity but long periods of stagnation, mainly because sales growth has not kept pace with peers.

The valuation today suggests investors are willing to wait, but not indefinitely. If Emami can lift annual earnings growth to even 10-12 percent through stronger sales, the current multiple could look reasonable.

But if growth continues in the low single digits, the stock may remain a “value trap”, basically a solid, profitable company, but not a rewarding investment.

In simple terms, management is betting on brand refreshes, digital channels, and a better consumption environment to bring back growth. The stock trades cheaper than its peers, but that is because the market does not yet believe in a strong growth story. For investors, the upside will only come if Emami can prove that its next decade will look different from the last.

Note: This article relies on data from annual and industry reports. We have used our assumptions for forecasting.

Parth Parikh has over a decade of experience in finance and research and currently heads the growth and content vertical at Finsire. He holds an FRM Charter and an MBA in Finance from Narsee Monjee Institute of Management Studies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.