Is the TCS slowdown a buying opportunity? | Smart Stocks News

Tata Consultancy Services (TCS), the largest IT services stock on the NSE and the most valuable company under Tata Sons, paid its highest-ever dividend in FY25. Despite this, TCS shares underperformed the broader market, falling 16% year-to-date, while the Nifty 50 Index rose 3.27%.

This underperformance wasn’t isolated. The entire IT sector witnessed a downturn, with the Nifty IT Index declining 14.6% amid weak global macroeconomic indicators, especially in the United States, which accounts for nearly 70% of India’s IT export revenue.

Fears of a recession in North America slowed revenue growth for several IT services companies with high exposure to the US. The recent downgrade of the US long-term issuer and senior unsecured ratings by Moody’s from AAA to Aa1 has only deepened concerns about a delay in the recovery of India’s IT sector, signaling slow revenue and earnings growth for FY26 as well.

TCS’s revenue growth in FY25 was largely driven by a significant contract with BSNL. With revenue from this deal ramping down, there are concerns about how TCS will fill the revenue gap in FY26.

A slowdown in revenue could also impact TCS’s dividend per share. But why is that such a big deal?

The importance of TCS’s dividend to Tata Sons

TCS is the crown jewel in the Tata Sons portfolio and its largest dividend contributor. Tata Sons owns 71.7% of TCS, and in FY24, TCS paid Rs 18,958 crore in dividends, accounting for 88% of Tata Sons’ total dividend income. In FY25, this figure rose to Rs 44,962 crore, of which Tata Sons is estimated to have received Rs 32,269 crore.

Dividends from TCS represent 49% of Tata Sons’ standalone revenue TCS dividend and share buyback accounted for ~92% of Tata Sons’ operating income during the FY17-FY24 period.

Story continues below this ad

Source: Tata Sons FY24 Annual Report

Source: Tata Sons FY24 Annual Report

Tata Sons uses the income received from its holdings to invest in new businesses, such as the funding for the turnaround of Air India, the Rs 91,000 crore Dholera semiconductor fab first plant project, and the Rs 27,000 crore Assam semiconductor ATMP project.

In FY24, TCS’s dividend and buyback proceeds helped Tata Sons to repay all its debt and avoid the need to list on the stock exchanges, giving it the flexibility to undertake high-risk, capital-intensive projects.

The significance of TCS dividends in Tata Sons’ finances makes one wonder whether a slowdown in TCS earnings could spell concern for Tata Sons.

Outlook for TCS dividends

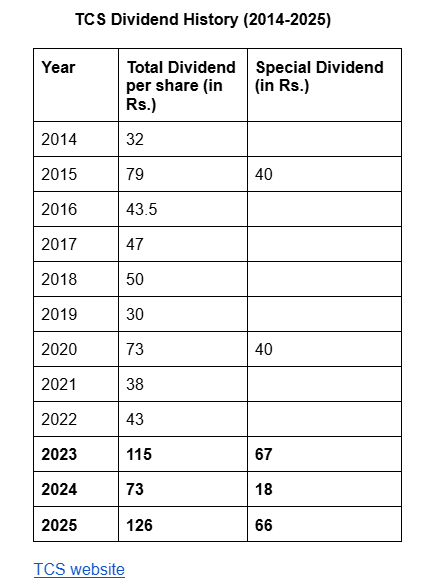

Analysing the trend of the last 10 years, TCS revenue growth has slowed in FY18 (the US-China trade war), FY21 (pandemic), and FY24 (recession fears). The slowdown in revenue growth led to a decline in dividends paid as earnings fell.

Story continues below this ad

Each time, the company rebounded strongly. After the pandemic-induced slowdown in FY21, TCS saw a 16-18% revenue growth over the next two years.

It saw strong deal momentum in FY24, with total contract value (TCV) up 25% to $42.7 billion as global macro outlook showed signs of improvement with disinflation and monetary easing, supporting growth. While there was continued pressure on discretionary spending, cost optimisation and cloud transformation projects led the deal momentum.

However, macroeconomic headwinds resurfaced after Trump’s retaliatory tariffs, which pulled down TCS’s order book by 8% in FY25. The company believes this uncertainty is temporary and FY26 could be better than FY25. At Q4 FY25 earnings call, K Krithivasan, CEO, TCS, said the company will start investing more in technology transformation or technology adoption once uncertainty clears.

The last 10-year trend shows TCS has remained resilient to macroeconomic headwinds and consistently paid dividends. It even paid a special dividend for three years in a row for the first time since its IPO.

Story continues below this ad

One possible reason for the special dividend could be that the slowdown in the US was partially offset by strong growth in India, where TCS has been involved in nation-building transformation projects.

Can India’s IT spending bridge the gap made by the slowdown in US IT spending?

Ever since TCS was formed, IT services exports, especially to the US, have been driving India’s IT stocks. Trump’s retaliatory tariffs were not directly targeted at IT services, hinting at the importance of IT service exports to both countries. However, tariffs in other sectors could increase costs for clients in retail, airlines, travel, and hospitality, and reduce their IT budgets, which could indirectly impact the revenue of IT service companies.

In the meantime, government spending on IT is driving demand in India. Gartner forecasts India’s IT services spending to grow 11.4% in 2025 from 8.8% in 2024 and 4.8% in 2023. TCS could benefit from this increasing spending. The company saw its revenue growth from India accelerate in the last three years, surpassing that of the US and Europe.

India’s fast-growing IT spending is bridging the gap created by the slowdown in the US IT spending. However, India is still a long way from bringing its IT spending to the level of the US and emerging as a key market for IT services.

Story continues below this ad

What could be the next big opportunity for TCS?

According to K Krithivasan, two new growth opportunities could open up in the medium to long term, once tariff uncertainties settle:

- Application of ‘AI for IT’ and ‘AI for Business’

- Tech transformation from the expensive legacy infrastructure to cost-efficient cloud.

Like every technology trend, AI will first disrupt the current IT service market and then create opportunities in new areas. TCS is approaching these new areas in three ways:

- Building on industry-specific AI and data solutions to be relevant to business

- Building scale through strategic partnerships and a unified platform approach

- And emphasising Responsible AI and data governance

Could a slowdown in TCS earnings concern Tata Sons?

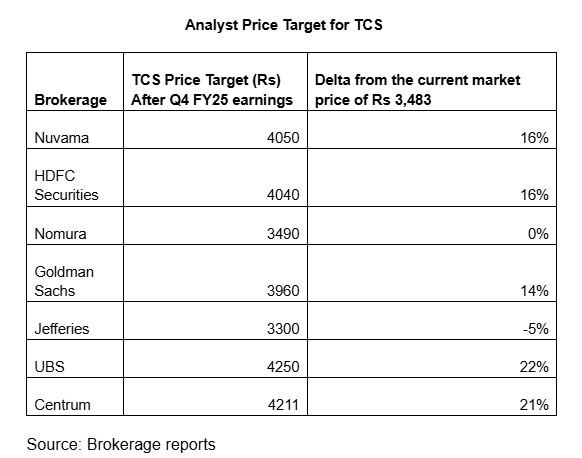

While it is true that these are challenging times for the IT sector, the concerns of TCS earnings slowdown are perhaps overblown. TCS share price is down 22% from its December 2024 high and is trading at a 25.8x price-to-earnings (P/E) ratio, which is below its 10-year median of 26.7x and sector median of 30.28x.

Brokerages have reduced their price target for TCS in light of a weak demand environment amid global macroeconomic uncertainty. However, some brokerages such as Centrum remain optimistic for the medium-term as they expect demand to be driven by strong GenAI deal momentum.

Story continues below this ad

To answer the question, could a slowdown in TCS earnings concern Tata Sons in the short term? Yes. However, the current slowdown could be considered a step back before taking a leap at AI opportunities.

TCS continues to remain a lucrative IT stock with 52.38% Return on Equity, which is higher than its peers (Infosys – 28.8%, HCL Tech – 25%). It is an interesting stock to add to your watchlist, as it is well-positioned to benefit from increasing domestic demand and the technological shift to cloud.

Note: We have relied on data from http://www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Puja Tayal is a financial writer with over 17 years of experience in the field of fundamental research.

Story continues below this ad

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.