EID Parry: The curious case of a ₹14,000 crore stake hidden in plain sight | Smart Stocks News

EID Parry has long been a steady presence in the market — a company that has quietly built its legacy over the years.

Its journey may seem unassuming at first: over the past five years, it has delivered a respectable 29% annual return (CAGR), and today, it is valued at about ₹15,000 crore. But beneath this modest market cap lies a surprising twist.

EID Parry holds a 56% stake in Coromandel International, a leading name in the agri-chemicals sector, with a total market cap of ~₹56,000 crore.

In simple terms, in EID’s books, this stake in Coromandel alone is worth roughly ₹31,000 crore — more than double EID Parry’s entire market value.

This striking contrast raises an important question: Is the market fully recognising the true potential of EID Parry? While its headline numbers might suggest a steady performer, the hidden treasure in its portfolio hints at a much larger story, one where significant upside could be waiting to be unlocked.

Stock price movement of EID Parry (India) Ltd. (Source: Screener.in)

Stock price movement of EID Parry (India) Ltd. (Source: Screener.in)

Unveiling the hidden 250%: EID Parry’s underlying transformation

EID Parry has built its legacy on solid, traditional businesses that have weathered market cycles with steady performance. Over the past five years, its core operations — primarily in sugar production and nutraceuticals — have provided the stability and cash flow that form the backbone of the company.

1. Sugar: The old reliable

Story continues below this ad

Sugar has long been the bedrock of EID Parry’s operations.

With six modern mills across South India and a combined cane crushing capacity of around 40,800 tonnes per day, the sugar business remains a steadfast, if not flashy, contributor.

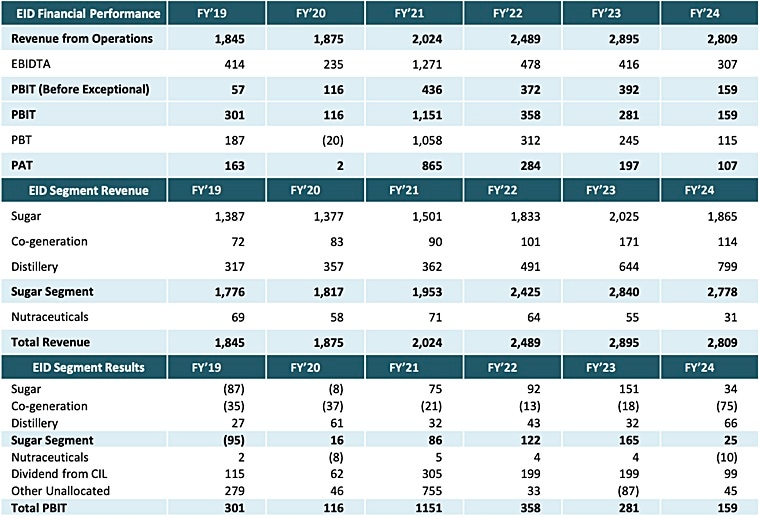

In FY24, the sugar segment generated roughly ₹1,865 crore in revenue. However, this business isn’t without its challenges. Regulatory interventions, such as export restrictions, mandated cane pricing, and government-imposed blending targets, often squeeze margins into sub 6% range.

2. Co-generation: Turning byproducts into power

Story continues below this ad

The co-generation business takes what might otherwise be a waste product — bagasse, the fibrous residue from sugarcane — and transforms it into a valuable asset.

EID Parry’s integrated sugar mills are equipped with cogeneration units that together produce around 140 MW of power. This segment not only meets the internal energy needs of the mills but also generates surplus electricity, which is sold to the grid or private players.

Though the revenue figures for co-generation are smaller compared to sugar (contributing a steady, supportive income stream), the business has evolved as a critical piece of the sustainability puzzle.

3. Distillery: Fueling growth with ethanol

The distillery business is where EID Parry leverages its core commodity to tap into the high-growth green energy sector.

Story continues below this ad

Operating through five distilleries with a current capacity of 582 KLPD, the distillery segment is responsible for producing around 60 million litres of ethanol annually. In FY24, this segment generated approximately ₹799 crore in revenue.

Ethanol production offers margins — typically in the sub 7% range — similar to the sugar business. The strategic shift to prioritise ethanol, driven by government initiatives to blend ethanol with petrol, has allowed the distillery business to not only offset some of the inherent cyclicality of sugar but also to act as a growth engine.

4. Nutraceuticals: A dash of health

As consumer preferences shift toward wellness and organic products, EID Parry has branched into the nutraceuticals space.

This segment, though modest in scale compared to sugar, has garnered attention for its higher-margin potential. In FY24, nutraceuticals generated around ₹31 crore in revenue.

Story continues below this ad

Products such as spirulina tablets and other organic supplements exemplify the company’s commitment to quality and innovation in health and wellness. While growth here has been variable, the strategic importance of nutraceuticals lies in diversifying revenue streams.

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation/May 2024)

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation/May 2024)

5. Consumer Products: From bulk to branded

Traditionally known as a bulk sugar manufacturer, the company is now positioning itself to capture the premium retail space. This involves transitioning from selling commoditised sugar into offering a range of branded products, such as value-added sweeteners, supergrains, and other processed food items.

Though still in its nascent stage, the consumer products segment is rapidly progressing. Recent initiatives include the launch of branded sweeteners and packaged supergrains that aim to tap into the fast-growing Indian FMCG market.

Story continues below this ad

By expanding its distribution — from a few thousand outlets to over 1 lakh retail touchpoints — the company is working to secure a more profitable and resilient revenue base. This shift is designed to unlock premium pricing and reduce the dependency on fluctuating commodity prices, signaling a new chapter in EID Parry’s long history.

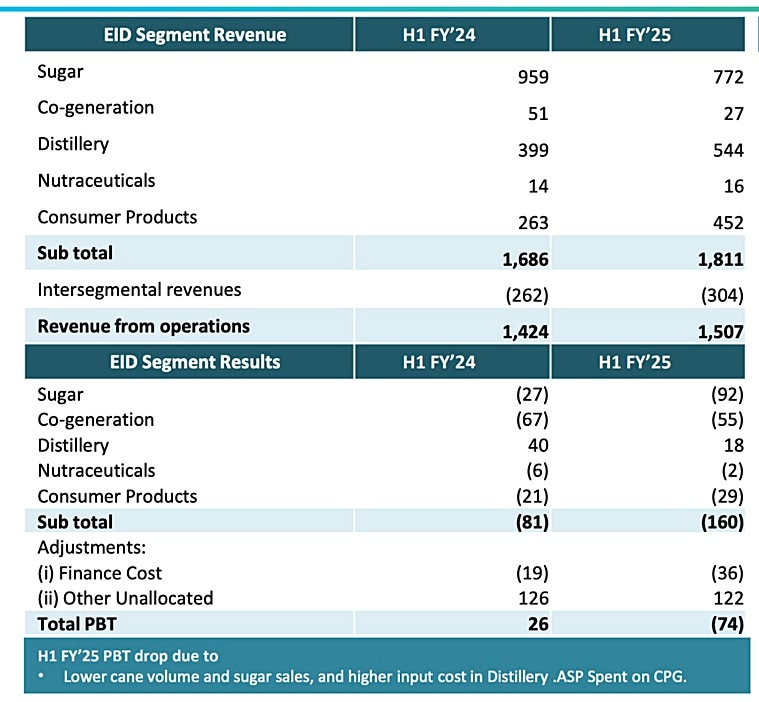

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation/Nov 2024)

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation/Nov 2024)

Valuation analysis: Sum‐of‐the-parts versus market discount

To understand the disparity between market perception and fundamental value, we first need to examine the individual components of EID Parry’s business.

The sugar division, historically the company’s mainstay, continues to generate consistent revenues, reporting ₹1,865 crore in FY24. However, sugar is an inherently volatile industry, subject to government pricing policies, export restrictions, and unpredictable weather conditions. Despite these challenges, the business remains a crucial part of India’s agricultural landscape. Globally, sugar companies trade at price-to-earnings (P/E) multiples of around 9x, and even with subdued profitability, EID Parry’s sugar business could be conservatively valued at ₹300-400 crore.

Story continues below this ad

Beyond sugar, EID Parry has been steadily leveraging its by-products.

The co-generation business, which converts bagasse into renewable energy, contributes to operational efficiencies. However, this segment reported a PBIT loss of ₹75 crore in FY24, reflecting operational inefficiencies or non-cash adjustments. While the revenue from this segment stood at ₹114 crore, its valuation remains subdued, estimated at ₹100-200 crore, primarily based on future energy sales potential rather than current earnings.

The real game-changer within EID Parry’s core operations is its distillery business, which focuses on ethanol production. With the Indian government aggressively pushing for ethanol blending in fuel (targeting 20% by 2026), companies in this space have witnessed improved pricing power and margins.

EID Parry’s distillery segment recorded ₹799 crore in revenue in FY24, supported by reasonable margins, making it the most profitable standalone segment. Globally, ethanol businesses trade at higher multiples, around 12x earnings, suggesting a valuation range of ₹750-900 crore.

Story continues below this ad

Then comes the nutraceuticals division, which, despite its relatively small contribution to overall revenue, holds significance due to its higher-margin profile. However, FY24 saw a sharp decline in segment profitability, with a PBIT loss of ₹10 crore. This decline may be temporary, but it highlights the challenge of scaling operations in India’s fragmented wellness market. Even with fluctuating performance, nutraceuticals tend to attract premium valuations due to long-term demand trends, leading to a valuation range of ₹200-300 crore.

Lastly, EID Parry’s consumer products segment represents an effort to move beyond bulk sugar sales into the branded retail space. This shift, if executed well, could allow the company to command higher pricing power and improve earnings stability. Though early-stage, a valuation estimate of ₹300-500 crore can be assigned, assuming moderate traction in premium sugar and wellness-based consumer products.

When aggregated, these core business segments contribute to a conservative standalone valuation of around ₹3,000 crore, which, while modest in isolation, underscores the strength of EID Parry’s diversified operations.

The Coromandel connection: A ₹31,000 crore undervalued asset?

What makes EID Parry unique isn’t just its core business — it’s the fact that it owns a 56% stake in Coromandel International, a dominant player in India’s fertiliser and agro-chemicals industry. Over the past five years, Coromandel has grown at a 24% CAGR, and today, the company boasts a market capitalisation of ₹56,000 crore. This means that EID Parry’s stake alone is worth nearly ₹31,000 crore, more than double its own market capitalisation of ₹15,000 crore.

This massive discrepancy is hard to ignore.

If an investor were to buy EID Parry today, they would effectively be getting its entire sugar, ethanol, co-generation, nutraceuticals, and consumer business for free, while still paying less than the full value of its Coromandel stake. Even after applying a holding company discount of 50-60%, EID Parry’s fair value should be at least ₹18,000-22,000 crore, still higher than where it currently trades.

Why the deep discount?

The persistent undervaluation of EID Parry can be attributed to several key factors:

Holding company discount

- Holding companies in India typically trade at a 50-60% discount due to concerns over capital allocation, lack of direct control over subsidiary cash flows, and the reluctance of management to unlock value.

- Investors often prefer to buy Coromandel shares directly, rather than purchasing EID Parry and indirectly owning Coromandel.

Cyclicality of the sugar business

- While EID Parry has been expanding into ethanol, nutraceuticals, and branded consumer products, the sugar segment remains volatile.

- The industry is highly regulated, with government-imposed cane pricing, ethanol blending mandates, and export restrictions impacting profitability.

Trading liquidity concerns

- While Coromandel trades with a daily volume of ₹250 crore, EID Parry’s daily trading volumes are only ₹30-40 crore, making it less attractive for large institutional investors.

Murugappa Group’s conservative approach

- The Murugappa family, which owns EID Parry, is known for long-term stability over aggressive financial engineering.

- Historically, they have not pursued spin-offs or stake sales, which frustrates investors looking for near-term catalysts.

The investment opportunity: Is there money to be made?

At its current market capitalisation of ₹15,000 crore, EID Parry is being valued as if its standalone businesses (sugar, ethanol, co-generation, nutraceuticals, and consumer products) are barely worth anything.

Assuming the standalone businesses are conservatively valued at ₹3,000 crore, that leaves the implied valuation of its 56% Coromandel stake at just ₹12,000 crore — a 60% holding company discount from its fair market value of ₹31,000 crore.

While a 50-60% discount is high, it is not unusual in the Indian market for holding companies, especially those with diversified businesses and a history of conservative capital allocation. However, for investors to see meaningful upside, the following triggers would need to materialise:

Narrowing of the holding company discount

- A partial or full spin-off of Coromandel International would force the market to assign a fairer value to EID Parry’s stake.

- If Murugappa Group monetises a portion of its Coromandel stake, either through stake sale or dividend distribution, it could reduce the discount significantly.

Ethanol expansion and higher profitability in standalone business

- The government’s 20% ethanol blending mandate by 2026 presents a major growth opportunity for the distillery segment.

- If EID Parry’s ethanol revenue and margins improve, it would lift standalone profitability, making the business more attractive.

Debt reduction and capital restructuring

- EID Parry’s net debt is manageable, but a further reduction in debt levels (either through Coromandel dividends or operational cash flow) could improve investor sentiment.

- A buyback or special dividend from Coromandel’s cash flow could also serve as a value-unlocking move.

Conclusion: A deep value play that needs a catalyst

At a 60% holding company discount, EID Parry’s valuation is stretched to the higher end of the Indian market range. While such discounts aren’t abnormal, they indicate that the market is deeply sceptical of immediate value unlocking.

For investors, the key question is: Will this discount persist, or will one of these catalysts trigger a re-rating? If any of the above scenarios materialise, EID Parry could see an upside as its discount narrows toward the lower end of the typical holding company range (40–50%).

While patience is required, the combination of Coromandel’s steady growth, ethanol-driven profitability improvements, and potential corporate restructuring makes EID Parry a deep-value opportunity with asymmetric upside. Only time will tell whether this ride towards unlocking will turn out to be sweet as well.

Note: We have relied on data from the annual reports throughout this article. For forecasting, we have used our assumptions.

Parth Parikh has over a decade of experience in finance and research, and he currently heads the growth and content vertical at Finsire. He has a keen interest in Indian and global stocks and holds an FRM Charter along with an MBA in Finance from Narsee Monjee Institute of Management Studies. Previously, he has held research positions at various companies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.